Attention set firmly on key central bank meetings next week (Fed, ECB and BoJ) meant that it was a relatively quiet week for markets. Some strength returned to the US dollar as activity data in China disappointed. Meanwhile, an improved UK inflation report saw the FTSE index rising more than 3% on the week, with markets now pricing a materially lower peak interest rate from the BoE. These dynamics offshore drove a lower Australian dollar, outweighing a rise in expectations for another RBA rate hike on the back of strong labour market data.

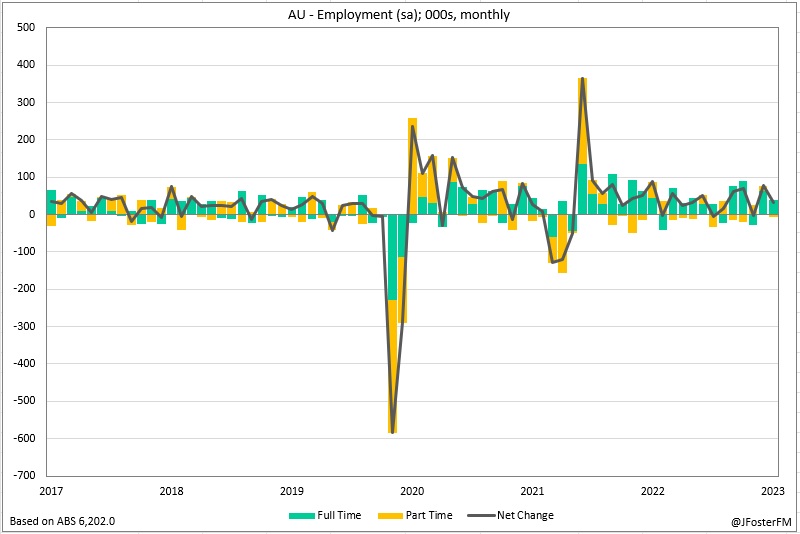

After finding renewed momentum in May, the Australian labour market showed further strength in June (reviewed here). Employment increased by 32.6k, well above the 15k consensus and coming off the back of the strongest rise in 11 months in May (76.5k). Robust labour demand saw the unemployment rate hold around half-century lows at 3.5% (unchanged from May) as labour force participation - despite easing 0.1ppt to 66.8% in June - remained around record highs. Rapid post-pandemic inward migration is clearly adding to labour supply but also appears to be supporting employment as well. Momentum in employment growth was a solid 3.1% annualised in the June quarter, a pace that exceeded growth in the labour force on an equivalent basis (2.8%).

The June report saw pricing for an RBA rate hike in August jump to around 40% from 25% pre-release. While the Board left rates on hold earlier this month, the meeting minutes outlined that a 25bps hike had come under consideration, mainly due to risks to the inflation outlook. However, the Board elected to hold, seemingly awaiting next week's Q2 CPI report. The minutes noted that the July hold came as the discussion around the Board table focused on the balance of risks between under-tightening and over-tightening. Interest rates were assessed to be "clearly restrictive" at 4.1% and policy lags meant the full effects of the tightening cycle had yet to play out. However, the Board remains alert to inflationary risks stemming from the services sector and labour cost pressures associated with the strong labour market.

---

In a relatively quiet week offshore, key data from China came in on the soft side of expectations as the momentum from the Covid reopening showed further signs of fading. June quarter GDP slowed to 0.8% from 2.2% in Q1, leaving year-ended growth at 6.3% against 7.1% anticipated. Retail sales (3.1%yr) also disappointed, but an upside result came through for industrial production (4.4%yr).

Over in the US, while headline retail sales at 0.2% in June missed expectations (0.6%), control group sales - considered a better gauge of underlying spending - posted an upside surprise rising by 0.6% (vs 0.3%). Resilience in US consumer spending remains evident supported by a strong labour market and improved purchasing power from real incomes with inflation cooling materially.

Declining UK inflation saw markets scale back pricing for a second consecutive 50bps rate hike from the Bank of England. Only last week, an acceleration in wages growth led to a 50bps hike coming close to being fully priced for the August meeting, but prospects for a 25bps increase received a boost after CPI data for June came in weaker than expected. Headline CPI (12-mth) slid from 8.7% to 7.9% (below the 8.2% consensus figure) and the core rate softened from 7.1% to 6.9% (vs 7.1%); June's month-on-month inflation outcomes (0.1% headline and 0.2% core) were the slowest since the start of the year. Encouragingly, services inflation showed tentative signs of easing (7.2% from 7.4%) while goods disinflation continued (8.5% from 9.7%).