Australian inflation declined from 7% to 6% in year-ended terms in the June quarter, a downside surprise on expectations (6.2%). Global disinflationary forces are becoming more evident in prices in Australia; however, domestic impulses to inflation from services prices have firmed further.

Consumer Price Index — Q2 | By the numbers

- Headline CPI was 0.8% in the March quarter, below expectations (1%) and down from a 1.4% rise in the previous quarter. Year-ended inflation fell from 7% to 6% (vs 6.2% expected).

- The average of the three underlying CPI measures was 0.9% quarter-on-quarter, softening from 1.3% in Q1. This lowered the annual pace from 6.6% to 6%.

- The key trimmed mean measure printed 0.9% for the quarter, below consensus (1.1%) and down from 1.2% previously. This left the year-ended pace at 5.9% (vs 6.0%) from 6.6%.

Consumer Price Index — Q2 | The details

Australian inflation posted its softest quarterly outcomes in nearly two years in the June quarter. The headline CPI slowed to 0.8% quarter-on-quarter from 1.4% in the March quarter, while the key gauge of underlying inflation (trimmed mean) eased to 0.9%q/q from 1.2%. Year-ended inflation declined from 7% to 6% on headline, a low back to Q1 2022, while the core rate came down from 6.6% to 5.9%, its slowest in a year.

The easing of inflation in the June quarter was driven by price falls in domestic holiday travel (-7.2%) - associated with off-peak discounting; electricity (-1.8%) - reflecting state government rebate schemes; and fuel (-0.7%) on lower diesel prices.

The main contributors adding to inflation in Q2 were: rents (2.5%) - its strongest quarterly rise since 1988 reflecting very low capital city vacancy rates; overseas holiday travel (6.2%) as demand for summer travel in Europe surged; and eating out and take away services (7.7%) with these businesses passing higher costs (food and overheads) through to customers. While durable goods had contributed to lower inflation in the March quarter, a reversal of price discounting by retailers and new winter stock saw higher prices for furniture (4.9%) and clothing and footwear (0.6%).

Now at 6%Y/Y, headline inflation in Australia is down from a peak of 7.8% at the end of 2022. This decline largely reflects disinflationary forces from offshore - eased supply disruptions in goods and commodity markets and softer demand - with headline inflation rates in many advanced economies down significantly from last year's highs.

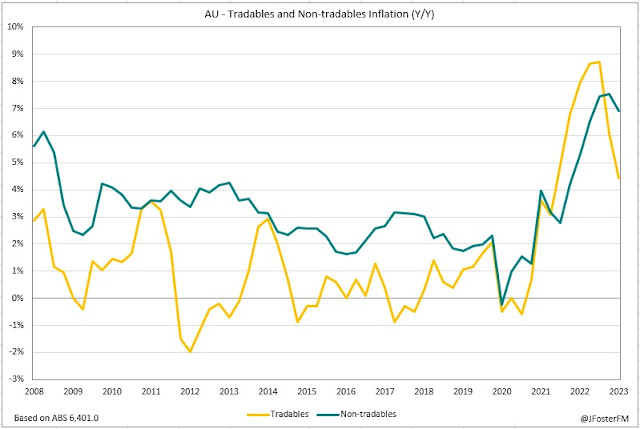

Because of this global disinflationary backdrop, the drivers of inflation in Australia are switching from global to domestic sources. Tradables inflation (goods and services prices influenced by supply-demand dynamics offshore) slowed from 6.1% to 4.4%Y/Y. That compares to non-tradables inflation (prices determined by domestic factors) at 6.9%Y/Y, though this looks to have peaked having fallen from Q1 (7.5%).

The main theme playing out in Australian inflation is similar to what is occurring offshore: goods inflation is slowing rapidly but services inflation is remaining more persistent. Goods disinflation gathered pace in the June quarter, with the goods CPI falling from 7.6% to 5.8%Y/Y, down from a cycle peak of 9.6%. In contrast, services inflation has yet to peak, firming from 6.1% to 6.3%Y/Y. A key aspect of services inflation is labour cost pressures stemming from the strong labour market.

Consumer Price Index — Q2 | Insights

A welcome decline in inflation in the June quarter, with Australia's headline (6%) and core rates (5.9%) coming in comfortably below expectations. These declines make things interesting ahead of the RBA's meeting next week. The Board could choose to extend its pause from the July meeting on the back of today's report or it could opt to hike by 25bps if it chooses to focus on the firming in services inflation. This shapes as another tight call, with risks that the decision could fall on the side of an August hike.