The RBA Board is set to hike rates by 25bps to 3.6% at today's meeting. The continuation of the tightening cycle in Australia follows the Board's shift to a more hawkish narrative at the February meeting. Markets responded by repricing the peak cash rate 50bps higher to around 4.2% currently.

A recap...

An upwardly revised outlook for inflation and wages growth prompted a more forceful tone from the Board when it met for the first time in 2023. It is now communicating that "further increases in interest rates will be needed over the months ahead..." to lower inflation back to the 2-3% target band.

The February statement removed the reference to rates not being "on a pre-set course" and the meeting minutes later revealed that the Board had taken a pause in rate hikes off the table, an option it had considered in December. Ultimately, the discussion came down to hiking rates by 25 or 50bps, which was resolved in favour of the former.

Today's meeting...

The tone of today's statement is key in light of the data received over the inter-meeting period. The December quarter national accounts last week reported that domestic demand stalled into year-end; household spending slowed as the post-pandemic rebound wound down and as disposable incomes were being squeezed by cost-of-living pressures and rising rates. These dynamics were broadly alluded to in February, so this is unlikely to have come as much of a surprise to the Board.

The other key aspect will be around inflation and wages. In February, the Board observed that "... the incoming data on prices and labour costs had tended to exceed expectations". Although the 12-month CPI declined from 8.4% to 7.4% in January, I think the Board will remain cautious in its assessment but continue to assert that Q4 was the peak for inflation.

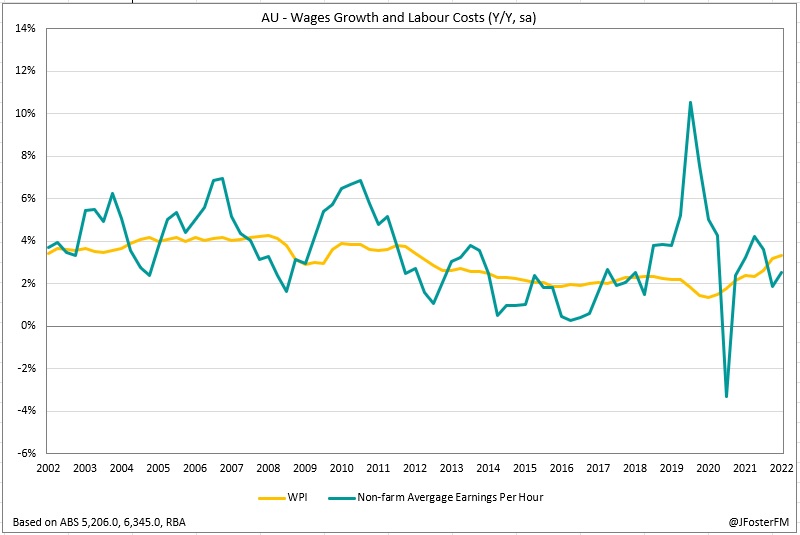

Where there could be some softening in tone is around wage pressures. The February statement emphasised the importance of avoiding a "prices-wages spiral"; however both wages growth (3.3%) and hourly labour costs have since been confirmed to be running below the RBA's expectations into year-end (3.5% and 4.7% respectively). That has come alongside a slight rise in the unemployment rate to 3.7%, though seasonal effects around December and January have made interpreting labour market conditions difficult.

Looking ahead...

Markets are priced for a peak in the cash rate at a little above 4%. Having only just made a hawkish tilt in February, the message for further rate hikes is likely to be reiterated. There could be some scope to soften the tone on the risks of a wage-price spiral emerging. Given the stalling in domestic demand in Q4, expect the RBA to retain the line about the narrow path to achieving a soft landing.