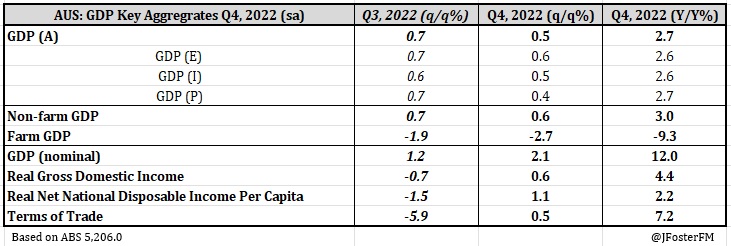

Growth in the Australian economy slowed to 0.5% in the December quarter, coming in below most estimates for around 0.8%. Growth through the year stepped down from 5.9% to 2.7%. Today's national accounts put the outlook for household consumption into 2023 under the spotlight; the post-pandemic recovery now looks to be complete and the headwinds from cost-of-living pressures and rising interest rates are still impacting.

There was a sharp slowdown in household consumption in the second half of 2022 (1.3%) from the first half (4.1%). In Q4, the pace weakened to 0.3% (5.4%Y/Y). The rotation in demand initiated by the full reopening of the economy was still unfolding, boosting services (1.2%) but weighing on goods (-1%).

The squeeze on household budgets caused by cost-of-living pressures has been historically significant, with real disposable income contracting by 2.2% over the past year. Consumption has been able to rise strongly in spite of that backdrop, supported by the reopening of the economy, more than $200bn of excess savings built up over the pandemic, and the strong labour market. However, high inflation has progressively made households worse off, reflected in the reduction in saving. In Q4, the household saving ratio declined from 7.1% to 4.5%, its lowest level in several years.

Rising interest rates have amplified cost-of-living pressures. Interest payment as a share of nominal disposable income lifted to its highest in 8 years (5.4%). This is only slightly above the 5% level seen in the years preceding the pandemic, but the pace of the move has been rapid, rising from a 3% share before the RBA's first rate hike in the current tightening cycle in May last year.

More broadly, the national accounts painted a picture of soft demand into year-end. Domestic demand growth stalled in the quarter on the back of soft household consumption (0.3%), weak business investment (-0.8%) and public demand that was little more than flat (0.3%).

Headline GDP growth was boosted by a substantial contribution from net exports (1.1ppt). However, this was due much more to declining imports (-4.3%) (which boosts GDP) than strength in exports (1.1%), consistent with that overall picture of soft demand.

More to follow.

.jpg)