The post-Covid expansion in the Australian economy continued into 2022 despite significant disruptions from the Omicron wave, severe wet weather events and supply constraints. Real GDP expanded by a stronger-than-expected 0.8% in the March quarter following an upwardly revised 3.6% rebound in the December quarter on reopening from the Delta lockdowns. Output through the year moderated from 4.4% to 3.3% but is still well above estimates of trend growth.

Australian GDP is now 4.5% above its pre-Covid level from Q4 2019, a significantly faster expansion than has been seen in advanced economies offshore (see below). Output remains a little below its pre-pandemic trajectory reflecting lower population growth associated with the closure of the international border throughout the Covid period.

Offshore, growth in the global economy slowed over the first quarter of 2022, while inflation pressures intensified following the emergence of new supply shocks. The Russian invasion of Ukraine and the return of lockdowns in China placed further strain on global supply chains, pushing up commodity prices, most notably for energy and food. With inflation continuing to rise, real household incomes were being squeezed in many countries, contributing to weakening sentiment. Recoveries in advanced economies were now broadly complete, with GDP having either cleared or returned close to their pre-pandemic levels of output.

In Australia, the surge of the Omicron wave of the pandemic and flooding across areas of New South Wales and Queensland disrupted activity during the quarter. This was reflected in national mobility indicators tracking a slower recovery from their seasonal fall for the Christmas/new year holiday than in 2021.

High vaccination rates avoided the lockdowns and associated restrictions seen in earlier waves of the pandemic; however, together with weather-related impacts, hours worked in the economy fell by 0.9% in the quarter.

Isolation rules for confirmed cases and for their household contacts led to widespread staff absences, while the severe wet weather events also saw many Australians working fewer hours in March. These disruptions came on top of ongoing supply chain pressures affecting firms.

The resilience of the economy was reflected in the labour market. The national unemployment rate fell to 3.9% in March, its lowest level since the early 1970s and broader measures of underutilisation returned to their lows from the previous cycle well over a decade earlier.

The tightening labour market, accumulated savings and eased Covid restrictions were key factors that combined to overcome the disruptions in Q1 as well as falling consumer sentiment due to a further squeeze on real incomes from high inflation. As a result, household consumption advanced at a robust 1.5%q/q pace to drive GDP growth in the quarter. Public demand contributed a strong 0.7ppt to activity, supported by flood recovery and pandemic-related spending. Residential construction and business investment continued to be held back by capacity constraints, with Omicron and the wet weather causing further delays.

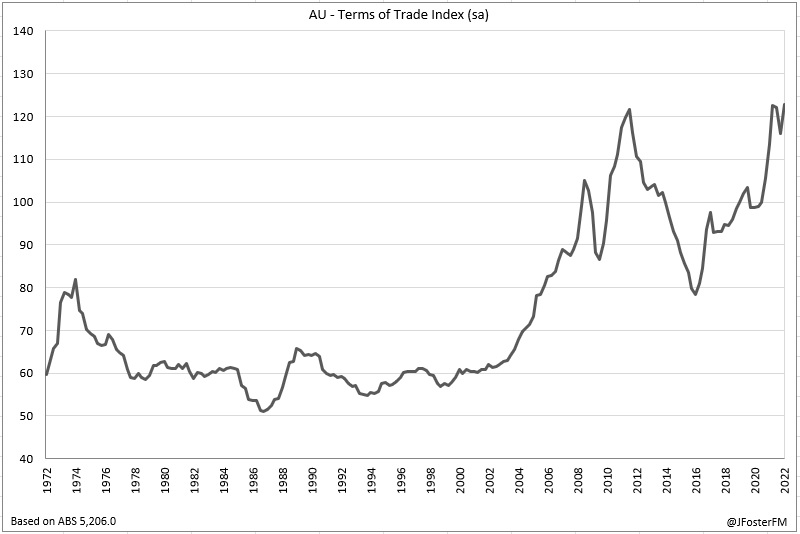

An easing in global supply chain pressures compared to the back half of 2021 supported the rebuilding of inventories (+1ppt) and enabled imports to flow into the country. With exports contracting due to the wet weather hitting resources and rural goods production (farm GDP fell by 6.7%q/q), net exports subtracted a sizeable 1.7ppts from GDP. However, with commodity prices surging in response to the Ukraine war, the terms of trade rose to a new record high, boosting national income.

The national accounts confirmed that wage-price pressures continued to rise over the March quarter. Hourly labour costs have lifted to be running above 5% in annual terms and key price deflator gauges accelerated, consistent with the surge in headline inflation to 5.2%Y/Y.

In response, the RBA is likely to raise its policy rate by 40bps at next week's June meeting having commenced its hiking cycle in May with a standard 25bps increase to 0.35%. This would return the policy rate to its pre-Covid level of 0.75%, with the strong expansion in the economy, the tightening labour market and rising inflation to confirm emergency support can be withdrawn.

— — —

National Accounts — Q1 | Expenditure: GDP (E) 0.8%q/q, 2.9%Y/Y

Household consumption (1.5%q/q, 4.0%Y/Y) — Australian household consumption was resilient amid the headwinds from the Omicron wave, severe wet weather events and rising inflation. Household consumption advanced by 1.5% in the quarter to be up by 4% through the year, supported by pent-up demand on a further easing of Covid restrictions, a tightening labour market and accumulated savings. This extended the momentum coming out of the reopenings from the Delta lockdowns where household consumption surged by 6.4% in Q4. Household consumption is now 2.5% above its pre-Covid level.

Discretionary spending lifted by 4.3% in Q1 to drive the increase in household consumption. On the back of this outcome, discretionary spending was now above its end-2019 level (+2%) for the first time in the Covid period. Essential spending was broadly flat in Q1 (-0.2%). Whereas the reopenings in Q4 led to similar rebounds coming through in goods (6.2%) and services consumption (6.5%), there was a pronounced rotation towards services in the March quarter as Covid restrictions on travel and at venues eased. Services consumption lifted by 2.3%q/q while goods consumption slowed to a 0.3%q/q rise. Overall, services consumption was still 1.5% down on its pre-Covid level while goods consumption remained at elevated levels, up 9.2% since the end of 2019.

The largest contributor to the rise in household consumption in the quarter was transport services (59.9%q/q) as border restrictions on domestic and international travel were eased. This drove an associated boost in consumption at hotels, cafes and restaurants (5.3%q/q), with venues also benefitting from loosened restrictions. A further return of crowds at sporting and cultural events lifted the recreation and culture category (4.8%q/q). Meanwhile, new vehicle purchases lifted by 13% in the quarter, rebounding from the delays in production that impacted delivery over the back half of 2021.

A tightening labour market led to wage incomes rising by 1.8% in the quarter. Following the floods, non-life insurance payouts surged (18.6%q/q). Together, these drivers led to a 0.6% rise in household disposable income in Q1, rebounding from a fall in Q4 (-0.5%). However, with inflation on the rise, real growth in household disposable income has contracted over the past couple of quarters (-1.2% in Q4 and -0.9% in Q1), with annual growth slowing to 1%. As a result, households have been spending out of accumulated savings over this period. The household saving ratio surged as high as 19.7% during the Delta lockdowns, before falling to 13.4% on the reopening. This retracement continued in Q1 to 11.4%, which is still a very elevated level but a notable development that highlights households were comfortable in spending out of accumulated savings despite the reported fall in consumer sentiment measures.

Dwelling investment (-1.0%q/q, -1.3%Y/Y) — Residential construction activity contracted for the second quarter running, with adverse weather adding to the delays stemming from labour and materials shortages. Activity fell by 1% in Q1 following the 1.9% decline in Q4, with these outcomes swinging growth into contraction in through the year terms (-1.3%).

New home building was down for a third quarter in succession; Q1's 2.2% fall is the largest over this stretch. After activity surged in response to the HomeBuilder scheme and other policy stimulus, new home building is now down by 5% from its recent peak in Q2 2021, with the sector running up against capacity constraints.

Some offset came through from a rebound in alteration work (0.7%q/q) following a decline in the previous quarter (-3.2%). Alteration work is at substantially higher levels than were seen immediately before the pandemic, up by almost 21%, reflecting the combined effects of policy stimulus and preference shifts for larger and improved homes.

In the established housing market, conditions in the nation's major capital cities in Sydney and Melbourne cooled during the March quarter. This contributed to ownership transfer costs — fees associated with real estate transactions — falling by 1.4% in Q1, though they have still risen by 7.7% over the year.

Business investment (1.4%q/q, 3.6%Y/Y) — The upswing in business investment alongside the economic recovery lost momentum over the back half of 2021 amid the Delta lockdowns and global supply chain pressures. The 1.4% rise in the March quarter has helped regain momentum, lifting business investment to 3.4% above its pre-Covid level. This was driven by the non-mining sector, with investment advancing by 2.4% in the quarter (5.3%Y/Y) to more than offset a 1.3% decline in mining investment (0.1%Y/Y).

Machinery and equipment investment picked up by 3.2% in Q1 to post its strongest outturn in a year. Government tax incentives, accommodative financing conditions and strong domestic demand had boosted demand for equipment investment, though this had stalled over recent quarters amid supply chain constraints. An easing of these pressures saw previously delayed purchases coming through. Non-residential construction was a point of weakness, with new building work contracting by 2.6%q/q as activity was held back by capacity constraints in the construction sector.

The recent ABS Capital Expenditure survey reported a strong uplift to investment plans for the 2022/23 financial year. The key is whether these intentions hold up as the global economy slows, with the outlook highly uncertain.

Public demand (2.6%q/q, 8.0%Y/Y) — After stalling in the previous quarter (-0.4%), public demand rebounded to advance by 2.6% in the March quarter to be 8% higher through the year. Consumption spending lifted by 2.7%q/q (8.3%Y/Y), boosted by the flood recovery effort and more pandemic-related spending through the acquisition of vaccines and R.A.T tests. Underlying investment broadly reversed Q4's decline (-2.3%) with a 1.6% increase; the outlook remaining supported by a vast pipeline of state government infrastructure projects brought forward to support the post-Covid recovery.

Inventories (1.0ppt in Q1, 0.7ppt yr) — Further rebuilding of inventories occured in the March quarter, adding 1.0ppt to quarterly GDP. This followed the progress made in the previous quarter, taking non-farm inventories back closer to pre-Covid levels. The major contributors to the rebuild in Q1 were the retail sector, with easing supply pressures boosting vehicle imports, and public authorities, reflecting the acquisition of Covid vaccines and R.A.T tests.

Net exports (-1.7ppts in Q1, -2.3ppts yr) — Net exports weighed heavily on activity, subtracting 1.7ppts from Q1 GDP. Exports contracted by 0.9%q/q, sliding to 13.6% below their pre-Covid level. The severe wet weather events during the quarter affected production in the resources and rural sectors, weighing on exports. After a weak second half of 2021, imports regained momentum with an 8.1%q/q surge, with volumes recovering to be 0.5% above their pre-Covid level. An easing in global supply chain pressures supported a rebound in imports of vehicles, household electrical goods and machinery and equipment in the quarter.

— — —

National Accounts — Q1 | Incomes: GDP (I) 0.8%q/q, 3.6%Y/Y

In the March quarter, the real GDP income estimate printed at 0.8%q/q, with growth through the year moderating from 4.7% to 3.6%. The main theme was the surge in national income driven by accelerating commodity prices in response to the war in Ukraine and other supply shocks. Nominal GDP lifted by 3.7% in the quarter, a touch higher than Q4's increase (3.5%), maintaining year-on-year growth at 10.2%. This latest surge takes national income to an extraordinary 15.4% above its pre-Covid level; output is up by 4.5% over the period by comparison.

A 5.9% lift in Q1 reset the nation's terms of trade to a new record high level. Export prices accelerated by almost 10% over the first quarter, with iron ore, coal, minerals and metals prices all rising at pace. Rising inflation in traded goods pushed up import prices by 3.5%q/q.

As a result of surging commodity prices, company profits lifted by 6% in the quarter (18.1%Y/Y), boosted by the mining sector. This was reflected in private non-financial corporations profits rising by a faster 7.3%q/q, accelerating annual growth from 10.6% to 21.6%. Also contributing to this rise was the wholesale industry on the pass-through of higher prices to consumers for petrol and vehicles. However, rising input costs crimped margins for manufacturers, weighing on aggregate corporate profits. A reduction in Covid-related fiscal support payments on the easing of restrictions led to declines in profits in the construction and hospitality industries, weighing on small businesses in particular with gross mixed incomes falling by 2.7% in the quarter. Financial corporations operating surplus lifted by 0.9%q/q to 5.4%Y/Y, with rising interest rates likely to boost net interest margins.

Reflecting the unwind of Covid-related fiscal support payments, taxes less subsidies on production and imports surged by 15.7% in Q1. Although this is partly driven by an increased tax-take from rising household consumption boosting GST and gambling revenues, subsidies on production fell by almost 40% in the quarter.

With the unemployment rate falling to its lowest level since the 1970s and the labour market seeing its tightest conditions in many years, compensation of employees advanced by 1.8% in Q1 to be up by 5.5% through the year. Hiring was robust, but hours worked fell during the quarter (-0.9%) due to the impacts from Omicron and adverse weather. With many workers having their pay linked to hours worked, average compensation per employee contracted by 0.7%q/q (2.2%Y/Y), while average non-farm compensation per employee fell by 0.8%q/q (2.1%Y/Y).

— — —

National Accounts — Q1 | Production: GDP (P) 0.7%q/q, 3.5%Y/Y

The GDP production estimate increased by 0.7% in the March quarter, with annual growth moderating back to 3.5% from 4.5%. Supported by eased Covid restrictions, gross value added (GVA) by the services sector of the economy lifted by 0.8% in the quarter, expanding to 5.3% above pre-pandemic levels. The goods sector also advanced by 0.8% in the quarter, but GVA is only 1.3% above pre-Covid levels, as supply chain pressures have held back the recovery.

In the services sector, business services GVA expanded by 1.2%q/q to extend the strength from the reopening in the previous quarter (3.3%q/q). This was driven by professional and technical services (3.1%q/q) on the back of rising demand for engineering, consulting and IT services, while financial and insurance services also advanced (0.7%q/q) amid the strong conditions in the housing market. Household services moderated in Q1 (0.3%) after surging post the Delta lockdowns (7.2%). The easing of Covid restrictions boosted the hospitality industry (3.7%) on a wider reopening of venues and on return to travel, while the arts and recreation industry (4.4%) benefitted from crowds returning to sporting and cultural events. These gains were moderated by healthcare (-0.9%q/q) on the suspension of elective surgeries due to the Omicron wave, and other services (-0.2%q/q) as repairs and maintenance works were delayed by staff absences due to Covid.

In the goods sector, GVA in goods distribution lifted by 2.7%q/q to 4.3% above their pre-Covid level. Eased restrictions on travel with borders reopening supported the transport industry (4.3%). Wholesale trade advanced by 3.2%q/q, benefitting from rising demand for mining, agricultural and transport equipment, and from an easing of supply chain pressures supporting motor vehicle dealers. Retail trade increased by 0.8%q/q on eased Covid restrictions. Goods production was soft in the quarter (-0.2%), easing back below pre-pandemic levels. This was driven by a 1.5% contraction in GVA from the mining industry, due to wet weather and Covid-related absences affecting production. Construction (0.2%q/q) was supported by work on backlogged projects, while utilities (0.9%q/q) advanced on increased demand for electricity in Victoria, Queensland and Western Australia.

— — —

National Accounts — Q1 | Prices

Both the GNE (gross national expenditure) and domestic demand deflators are not affected by the terms of trade, with these measures showing more moderate rises as a result. The GNE deflator was up 1.5%q/q to 4.2%Y/Y while the domestic demand deflator posted a 1.4%q/q rise to 4.1%Y/Y. Similar in concept to the CPI, though reflecting dynamic changes in purchasing patterns, the household consumption deflator broke out in the March quarter rising by 1.6%, its sharpest increase since the introduction of the GST in 2000. This left the annual pace up at 3.2% from 2.2%, a much more moderate rate than the CPI at 5.2%Y/Y, reflecting differences in methodologies with the household consumption deflator reflecting the effect of consumers switching to cheaper alternatives.

— — —

National Accounts — Q1 | States

State demand in New South Wales advanced by 1.2% in the March quarter, rising to be 3.8% higher through the year and now up 4.9% on its pre-Covid level. The drivers that supported demand were household consumption (1.9%) on the wider reopening of the services sector, while public spending (2.1%) was boosted by the flood recovery effort. Supply constraints weighed on non-dwelling construction, with business investment contracting over the year (-1.6%).

Victorian state demand continued to be supported by the reopening of the economy, expanding by 2.4% in Q1 (6%Y/Y), to be 5.4% above its pre-Covid level. Household consumption was up strongly (2.7%) on the back of Q4's initial reopening (7.5%); travel, dining out and attendances at sporting and cultural events surged on eased restrictions. Victoria was hardest hit by Covid lockdowns and as a result, business investment is in catch-up mode to the broader recovery, with strength coming through in the quarter in non-dwelling construction. Spending associated with the pandemic response continued to support public demand.

The other states have been much less affected by prolonged lockdowns, leaving expansions in state demand ranging between 7-9% above pre-Covid levels. In Queensland, state demand was up 0.8% on the quarter to 5%Y/Y. The response to the flooding in the south-east lifted public spending by 3.2% across the state and federal tiers of government. Tourism in the state is benefitting from the resumption of travel, driving a 0.4% increase in household consumption. Regarding business investment, activity in non-dwelling construction was hit by wet weather and supply constraints (-6%), though equipment spending was up sharply in Q1 (5.2%). State demand in South Australia was posted at 0.8%q/q and 4.7%Y/Y. Household consumption drove demand growth, rising by 0.9% in the quarter as eased restrictions supported tourism, with vehicle imports also up sharply. Business investment has expanded strongly over the year (7.4%) on the back of non-dwelling construction activity.

State demand in Western Australia advanced by 2.2% in Q1, its strongest rise in a year; however, public demand was the main driver, with Covid-related spending driving consumption (5.3%). Household consumption stalled in the quarter as rising virus caseloads weighed on spending at cafes and restaurants (-4.6%). Business investment lifted (3.4%) as equipment spending rebounded (14.8%) after contracting in the previous quarter. Tasmanian state demand declined (-0.6%) for the second quarter running, lowering growth through the year from 5.7% to 3.5%. Residential construction has been a key factor behind the slowing momentum following the end of the HomeBuilder stimulus and supply constraints in the sector. Household consumption declined in Q1 (-0.5%) driven by the health sector.