Australian retail sales posted their sharpest increase since the national reopening of the economy 18 months earlier surging by 7.3% in November. Eased restrictions in Victoria and Black Friday sales saw many Australians coming back to the shops in the lead up to Christmas. While Omicron has since emerged and already impacted spending, the experience from previous waves suggests the slow down should prove temporary as household consumption continues to have plenty of driving forces behind it.

Retail Sales — November | By the numbers

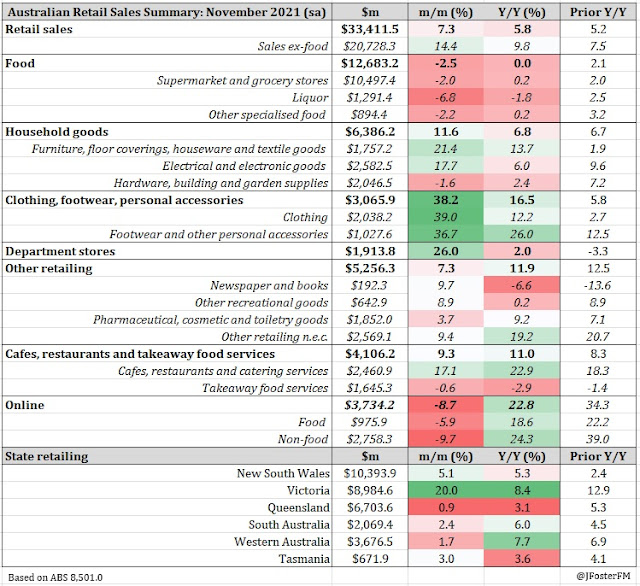

- National retail sales lifted by 7.3%m/m in November, more than double the expected rate of increase (3.6%), taking monthly turnover through $33bn for the first time on record. October sales advanced by 4.9%.

- 12-month retail sales firmed to a 5.8% pace from 5.2%.

Retail Sales — November | The details

With the nation emerging from the Delta wave, spending at the shops surged at its fastest pace since May 2020. November's 7.3% increase reflected the reopening in Victoria and a 'bring forward' effect ahead of Christmas from the Black Friday sales period and as people were encouraged to shop early to avoid availability and delivery concerns. With November turnover topping $33bn, this took Australian retail sales to 20.3% above pre-Covid levels. Highlighting the strength of discretionary spending, non-food sales soared by 14.4% month-on-month to be 27.6% above pre-pandemic levels of turnover.

Spending in Victoria increased by 20% in the month as the retail sector opened up more widely from its Delta restrictions and accounted for two-thirds of the rise in national turnover. Sales in New South Wales were up 5.1% following October's 13.3% reopening rebound. The ACT (19.2%) was also boosted by eased COVID restrictions. Much more moderate rates of increase were seen across the other states but sales remained at elevated levels having avoided harsh lockdowns during the Delta wave.

Category details were consistent with reopenings and the 'bring forward' effect ahead of Christmas. For the third consecutive month, basic food (-2.5%) fell as eating out (9.3%) increased, with the latter returning to pre-Delta levels. With people able to get out and about more and with Black Friday sales encouraging people back to the shops, clothing and footwear (38.2%), department store (26%), household goods (11.6%) and other retail spending (7.3%) surged.

Online sales contracted again (-8.7%) after falling in October, but turnover in the space is only just off the record highs during the Delta wave and at $3.7bn is vastly higher than the levels seen through 2020 to mid 2021.

Retail Sales — November | Insights

November sales confirmed that household spending was extremely strong coming out of the Delta wave. As seen in 2020, some of this spending in November was brought forward ahead of Christmas, encouraged by Black Friday sales. We could therefore see December sales fall back, but spending would still be at elevated levels. Looking ahead to January, retail foot traffic has seen a more pronounced slow down than 12 months ago, pointing to the effects of Omicron and that is likely to show up in weaker retail sales. However, there is little reason to think that the slowdown associated with Omicron would be anything more than temporary given the momentum seen after Delta and a household sector in strong shape supported by high accumulated savings and a tightening labour market.