Australian housing finance commitments rebounded by 6.3% in November after retracing from their stimulus-driven peak over recent months. The easing of lockdowns in New South Wales and Victoria looks to have been the key factor, supporting increases in owner-occupier and first home buyer activity, while investor commitments have hit a record high.

Housing Finance — November | By the numbers

- Housing finance commitments ($ value, ex-refinancing) increased by 6.3%m/m to $31.4bn (33.2%yr) against an expected flat (0.4%) outcome. Commitments are 3.4% off the May 2021 peak but are up 33.2% on a 12-month basis.

- Owner-occupier commitments ended a 5-month stretch of declines posting a 7.6% rise in November to $21.3bn for annual growth of 17.2%.

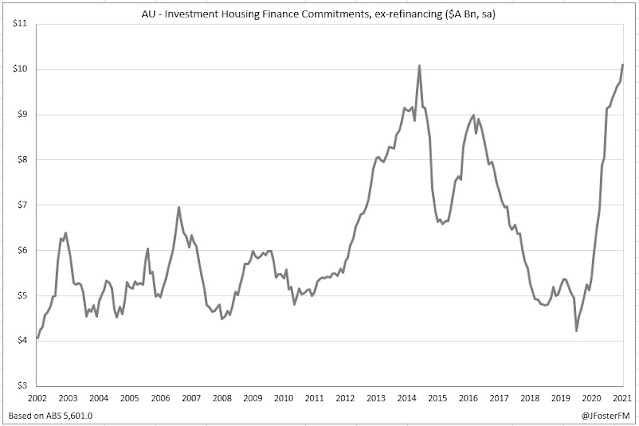

- Investment commitments reached a record high at $10.1bn after advancing by 3.8% in November (86.9%yr).

- Refinancing activity eased by a further 2.3% in the month but was still at an elevated level $15.7bn and up sharply on a year ago (55.1%) in a low interest rate environment.

Housing Finance — November | The details

Owner-occupier commitments had retraced by more than 15% from their May peak for the period through October but rebounded by 7.6% in November. The segment saw broad-based increases across upgraders (7.7%), first home buyers (3.7%) and in the construction-related category (6.3%).

The approvals data are broadly consistent with commitments. Upgraders rebounded from their recent slide, up 4.3% to 27,419. Both first home buyer and construction-related approvals are coming down from their cycle peaks following the withdrawal of the HomeBuilder stimulus but posted increases in November, the former rising by 1.9% to 11,622 as the latter advanced by 2.8% to 6,838 on an aggregated basis.

Commitments to the investor segment reset to a new record high in November at $10.1bn, surpassing the previous benchmark from April 2015. The segment has now sustained 13 consecutive monthly rises as low interest rates, rising housing prices and a gradual improvement in capital city vacancy rates have been supportive fundamentals.

In the refinancing market, commitments slowed over the month falling by 2.3% around declines of similar magnitudes in the owner-occupier (-2.1%) and investor segments (-2.5%). But the overall level of refinancing remains well above where it was pre-Covid. Clearly many borrowers are continuing to take advantage of low interest rates thanks to the RBA's measures including policy rate cuts and its bank term funding scheme as their fixed periods come to an end.

Turning to the states, the rebound in housing finance activity in New South Wales and Victoria post lockdown can be seen in the charts below (click charts to expand). This was most evident in the owner-occupier segment, helped by many first home buyers coming back to the market. However, the investor segment saw a more mixed picture as commitments elevated in New South Wales but held in their recent range in Victoria.

Housing Finance — November | Insights

The recent drift down in housing finance from the earlier peak in 2021 backed up in November as delayed activity during the New South Wales and Victorian lockdowns resumed. This supported a rebound in owner-occupier lending while investor commitments continued to lift resetting to a new record high in the process. However, with the support from stimulus fading following the end of the HomeBuilder scheme and with a shift to less accommodative policy from both a monetary and macroprudential perspective, expect housing finance to continue to trend down from elevated levels in 2022.