Australian housing finance commitments came in stronger than expected in May rising by 4.9% on the back of accelerating activity from the investor segment. Activity from owner-occupiers remains at elevated levels, though it is a nuanced picture in this segment between upgraders and first home buyers, with the latter seeing a reduction in stimulus from the end of the HomeBuilder scheme and house prices now sharply higher than at the time of the reopening a year ago.

Housing Finance — May | By the numbers

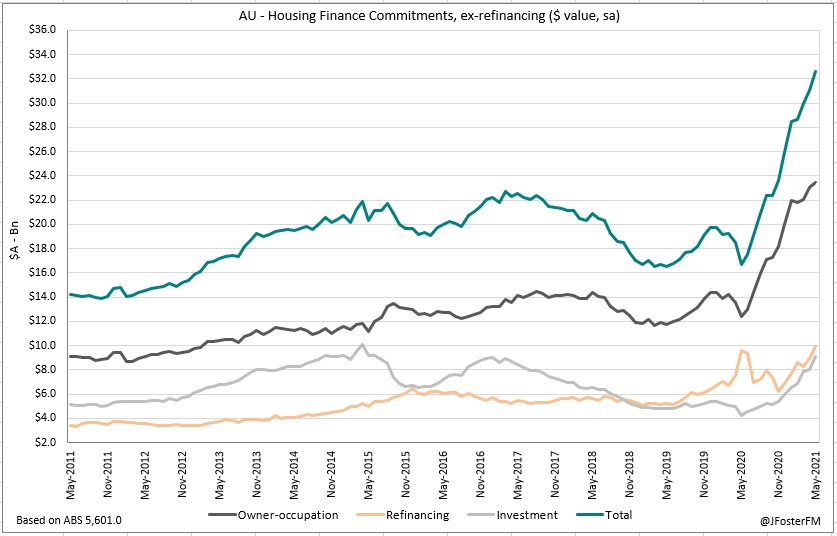

- Housing finance commitments ($ value, ex-refinancing) lifted by a stronger-than-expected 4.9% for the month in May to $32.6bn compared to the median estimate for a 1.8% rise. Annual growth accelerated from 68.2% to 95.4%, noting that the base period dates back to last year's trough amid the national lockdown and before many of the stimulus measures had been announced.

- Owner-occupier commitments increased by 1.9% in the month to $23.4bn to be up 88.4% over the year.

- Refinancing by owner-occupiers jumped 11%m/m to $9.9bn (2.7%yr).

- Investor commitments surged 13.3% in May $9.1bn (116%yr), reaching its highest level since June 2015.

Housing Finance — May | The details

Through the first two-thirds of the reopening period, owner-occupiers were driving the upswing with the stimulus measures being targeted at that segment, in particular first home buyers. With some of these measures now having wound down and with house prices having risen sharply, the driver of the cycle has pivoted to the investor segment. An improvement in conditions in many capital city rental markets is another key factor to highlight here.

In the owner-occupier segment, activity from 'upgraders' is continuing to rise (+3.6%mth, 95.4%yr) though commitments to first home buyers have plateaued (+2.5%mth), albeit at a very high level (+81.8%yr). Higher house prices leading to affordability concerns is likely to now be weighing on first home buyer activity.

The other factor behind the pivot from owner-occupiers to investors as the driver of the cycle is the expiry of the HomeBuilder scheme to new applicants at the end of March. Construction-related commitments (for new builds and to purchase newly built homes) made to owner-occupiers have rolled over from a peak of $5.7bn in February to $4.7bn in May. Loans for new construction have driven this, falling from $4.2bn to $3.1bn over the period.

The owner-occupier approvals data (by the number of commitments made rather than the value) reflect the themes discussed above. Construction-related approvals are now in decline, reflecting the unwinding of the 'frontloading' effect from the HomeBuilder scheme, while first home buyer approvals are coming down from their peak. However, set against this is the ongoing rise in approvals to 'upgraders', with higher house prices, strong household balance sheet and low rates enabling this group to remain very active in the market.

A summation of developments across the states is provided in the table below. Comparing the annual growth rates confirms the trend occurring at the national level, with investors taking over the running from owner-occupiers and, by extension, first home buyers.

As can be seen from this next chart, owner-occupier commitments are still at very high levels in all states. However, in recent months, the pace of increase has slowed in New South Wales and Victoria, while commitments have stopped rising in Queensland, Western Australia and South Australia.

Investor commitments are now accelerating, reflecting this segment's more delayed pick-up in this cycle, which appears to have needed an improvement in market fundamentals and for some of the incentives to owner-occupiers to have reduced.

Housing Finance — May | Insights

Today's report remained consistent with a very strong housing market, though it appears that as this cycle has progressed, investors are having an increasing influence with commitments in May reaching their highest level in nearly 6 years. Activity from owner-occupiers is still very strong, in particular from upgraders, but first home buyer activity is likely past its peak for this cycle with the HomeBuilder scheme having expired to new applicants and after the sharp rise in house prices over the past 12 months.