The RBA Board's first meeting for 2021 on Tuesday comes ahead of a busy week for Australia's central bank, with Governor Philip Lowe giving his usual 'Year Ahead' speech tomorrow (12:30PM AEDT) followed by Friday's parliamentary testimony (9:30AM AEDT) and later on that morning its quarterly Statement on Monetary Policy (SoMP) is published (11:30AM AEDT).

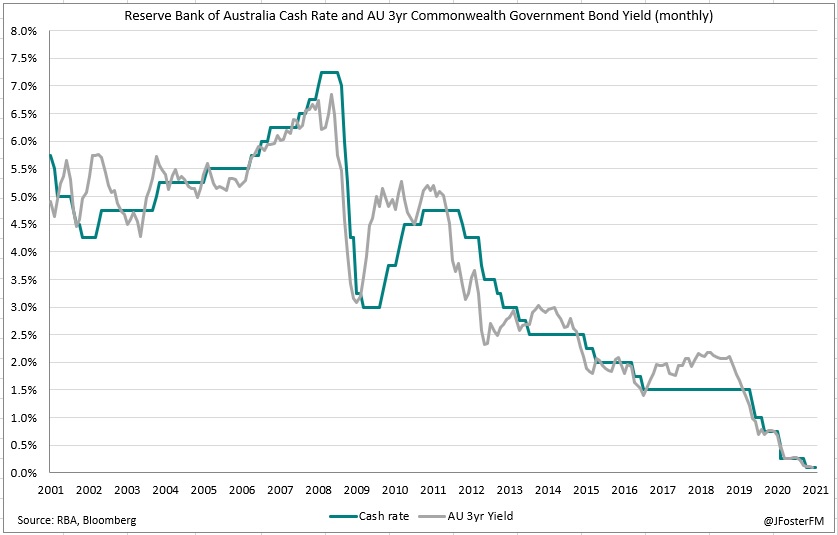

For today's meeting, no changes are expected to be made to the Board's monetary policy stance (0.1% targets on the cash rate and 3-year Australian government bond yield, 0.1% on Term Fund Facility drawings and $100bn bond purchase program) when Governor Lowe tables his decision statement at 2:30PM (AEDT). Since the Board last met in December, the data flow has generally come in strong reflective of an economic recovery that is running well ahead of the RBA's expectations, though the virus-related setbacks that have occurred in New South Wales, Brisbane and now Perth are a reminder of the risks the pandemic still poses.

The major changes will come in the RBA's forecasts that will need to be revised. This will be confirmed in Friday's SoMP, but today's decision statement may contain an outline of these revisions. Most notably, the unemployment rate ended 2020 at 6.6% compared to 8.0% anticipated back in the November SoMP and GDP growth after Q3's 3.3% outturn has the annual pace at -3.8%, which is already slightly better than where it was forecast to be (-4.0%) by the end of the year. However, do not expect better forecasts to signal a shift in tone from the RBA. With the Board's focus now explicitly on actual rather than forecast outcomes, expect Governor Lowe to reiterate the need for accommodative policy settings to be maintained until its employment and inflation goals are much closer to being achieved.

With a little more than half of the purchases ($52bn) under the $100bn bond purchase program now complete, there is rising interest on what the path forward might be. But at the current run rate ($5bn/wk) there is still plenty of time for these details to be forthcoming, with the $100bn target on track to be reached by around early April. Ultimately, an extension appears likely, though the RBA will probably want to avoid 'pre-committing' at this stage. The future of the Term Funding Facility may also come under consideration—ADIs have until the end of June to draw down on their additional and supplementary allowances—but again the details on this may come later down the line. Lastly, expect the cash rate and yield curve targets to remain in place for some time yet.