After the 0.3% decline reported in the March quarter, the level of Australian GDP has fallen to its lowest since Q3 2016.

After the containment measures were able to slow the infection rate, the National Cabinet announced a three-stage plan for reopening, which started to be enacted across most states from mid-May. A strong rebound in activity ensued, with around 39% of the earlier job losses recovered through the initial phase of the reopening. However, the recovery started to lose momentum in mid-June as virus concerns returned in Victoria, leading to an eventual reversal of its reopening, and this had spillover effects on confidence across the other states.

— — —

GDP — Q2 | Expenditure: GDP (E) -6.8%q/q, -6.0%Y/Y

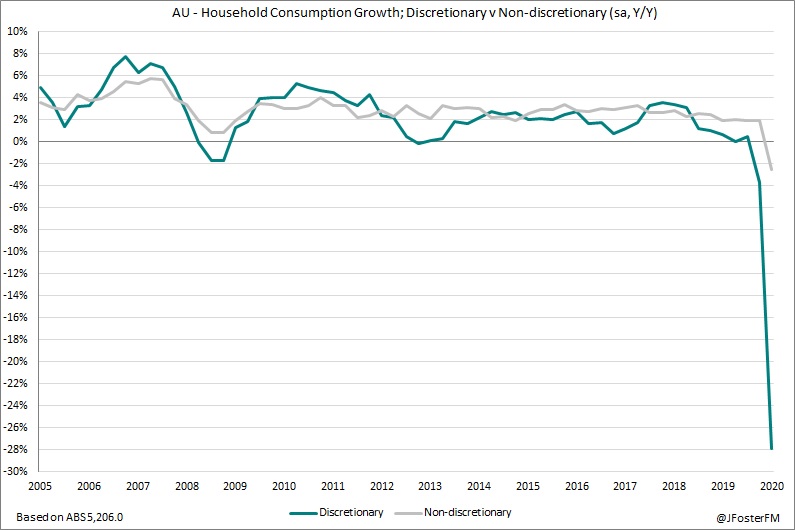

Household consumption (-12.1%q/q, -12.7%Y/Y) — Australia's historically large economic contraction of 7.0% in the June quarter centres on the household sector. The 12.1% collapse in household consumption accounts for 96% of the decline in economic output in Q2. This was a severely disruptive and unsettling period for domestic households with confidence collapsing to record low levels, while the labour market was upended as firms responded to the shutdown by standing staff down or cutting back hours.

Given the nature of the shutdown, the pattern of household consumption shifted very significantly and very rapidly. With large sections of the services sector shuttered and border closures grounding tourism, discretionary consumption collapsed. Very steep declines came through in the areas that were most impacted by the restrictions, such as transport services (includes travel) (-85.9%), hotels, cafes and restaurants (-56.1%), other services (such as personal categories) (-31.2%) and recreation and culture (-15.3%). Meanwhile, reduced mobility led to fuel consumption contracting by 25.5%. Areas of consumption that were well supported through the shutdown were in alcohol (13.0%) as licensed premises were closed and in household goods (9.5%) for entertainment purposes and to facilitate working from home arrangments.

The story around household incomes is very much linked to the Federal Government's fiscal support measures. The JobKeeper policy, enhanced unemployment support payments and cash flow assistance to businesses are estimated by the ABS to have added $48.0bn to household income over Q2, while the Bureau noted there was an additional $19.6bn not reflected in the national accounts through the early access to superannuation accounts and loan and rent deferrals. As a result of these measures, despite the dislocation that occurred in the labour market, real household income lifted by 3.0% in Q2 to its strongest pace in 9 years at 5.9%yr. However, with the shutdown restricting activity and with confidence having deteriorated, the household saving ratio soared from 6.0% to 19.8% — its highest since the mid-1970s. While the road to recovery is likely to be long and uncertain, the silver lining is that household balance sheets are now in strong shape and this will help support the nation through these troubling times, even as fiscal measures are eventually tapered.

Dwelling investment (-6.8%q/q, -11.2%Y/Y) — Residential construction has been in a downturn since the second half of 2018 and the 6.8% contraction that came through in Q2 was the weakest outturn over this period. New home building declined by 7.3% — its sharpest fall in 20 years — while alteration work pulled back by 6.0%. The impact of ongoing restrictions on migration and uncertainty around population growth dynamics is likely to lead to a more protracted recovery in the sector. Meanwhile, ownership transfer costs, which relate to fees associated with real estate transactions, collapsed by 18.6% in the quarter as turnover in the residential property market fell sharply in response to social distancing measures that prohibited open house inspections and public auctions.

Business investment (-3.5%q/q, -5.5%Y/Y) — The onset of the pandemic leading into the shutdown understandably saw business confidence collapse, as firms focused on preserving liquidity to make it through to the other side of the crisis. In response, business investment declined sharply across equipment and machinery (-6.8%) and intellectual property products (-6.0%), accelerating weakness already established ahead of the pandemic. The recent ABS Capital Expenditure survey pointed to a further declines in forward-looking investment plans, most notably in the services industries, given the highly uncertain economic outlook.

Business investment (-3.5%q/q, -5.5%Y/Y) — The onset of the pandemic leading into the shutdown understandably saw business confidence collapse, as firms focused on preserving liquidity to make it through to the other side of the crisis. In response, business investment declined sharply across equipment and machinery (-6.8%) and intellectual property products (-6.0%), accelerating weakness already established ahead of the pandemic. The recent ABS Capital Expenditure survey pointed to a further declines in forward-looking investment plans, most notably in the services industries, given the highly uncertain economic outlook.

Public demand (2.1%q/q, 6.3%Y/Y) — Robust public demand growth remains a key support for the domestic economy at a time of intense weakness in the private sector. Public spending lifted by a further 2.9% in Q2 (7.5%yr) as the health response to the pandemic ramped up. While investment has slowed of late falling by 1.6% in Q2 (1.1%yr), governments in Australia have indicated that infrastructure spending will be fast-tracked to support the economic recovery.

Net exports (1.0ppt in Q2, 1.6ppts yr) — Both exports and imports were severely impacted by pandemic restrictions, most notably those curtailing travel to and from Australia. Exports contracted by 6.7% in Q2, though a much larger fall was recorded by imports of 12.9% in which consumption of services collapsed by 50.5% as overseas travel was brought to a halt (-98.7%) by the international border closure, while capital goods (-2.5%) also weakened as business investment continued to deteriorate.

Inventories (-0.6ppt in Q2, -0.6ppts yr) — The disruption to operating conditions and weak demand conditions through the shutdown resulted in firms not needing to build up stock levels, with sharp declines in retail and wholesale inventories coming through.

— — —

GDP — Q2 | Incomes: GDP (I) -7.2%q/q, -6.4%Y/Y

The real GDP estimate of income posted a 7.2% fall in the June quarter as the annual pace plunged to -6.4% from 1.5%.

In nominal terms, Australian GDP contracted by 7.6% in Q2 — by a distance the largest quarterly income shock on record — to be down by 5.9% through the year as the shutdown hit business and employee incomes hard. However, this was mitigated by the transfer of subsidies from the Federal Government to the private sector.

The terms of trade were a negligible impact in the quarter, lifting by just 0.2% as the annual pace decelerated from -0.6% to -1.8% on a base effect.

Private sector company profits (ex-financial corporations) surged up by 14.9%in Q2 and by 16.3% over the year, with the key factors being the impact of the JobKeeper (wage subsidy scheme) and the 'Boosting cash flow for employers' (refund of tax withheld) policies. Small businesses were a key beneficiary of these policies with gross mixed income accelerating by 21.9% in Q2 to drive annual growth out of a 5-quarter long stretch in contraction to 19.6%. Financial corporations' profits weakened in Q2 falling by 0.5% (2.5%yr), with interest margins likely being squeezed by lower rates, while economic uncertainty weighed on credit demand in recent months.

Wages and salaries based on the compensation of employees measure declined by its most on record falling by 2.5% in the June quarter to cut 4ppts off the annual pace to 0.3%. However, the 2.5% contraction needs to be assessed against a fall of 9.8% in hours worked across the economy in Q2. Were it not for the JobKeeper policy, wages income would have fallen much more precipitously.

— — —

GDP — Q2 | Production: GDP (P) -7.1%q/q, -6.4%Y/Y

The June quarter production estimate contracted by 7.1%, with the annual pace falling to -6.4% from 1.5%. The impact of the shutdown was most severe on those operating in non-essential services, which were mandated by the Federal Government to close on March 22 or trade at a very restricted capacity, and also those in the travel and tourism industry in response to domestic and international border closures. As such, very large contractions came through from accommodation and food services (including licensed venues and hotels) -39.0%, arts and recreation (including sporting, gambling and performing arts activities) -22.6%, transport, postal and warehousing (including domestic and international travel) -21.5% and 'other' services' (such as hairdressers etc) -18.5%. Meanwhile, real estate services contracted by 15.9% due to the effective closure of the residential property market during the shutdown as open house inspection and public auctions were prohibited under social distancing guidelines.

Also of note, though construction was designated as an essential service enabling work to continue around social distancing guidelines, output still fell very sharply in Q2 (-8.2%), while the health care industry (-7.9%) was impacted by fewer face to face appointments and by reduced demand for hospital services. The full industry breakdown is outlined in the summary table, below.

Also of note, though construction was designated as an essential service enabling work to continue around social distancing guidelines, output still fell very sharply in Q2 (-8.2%), while the health care industry (-7.9%) was impacted by fewer face to face appointments and by reduced demand for hospital services. The full industry breakdown is outlined in the summary table, below.

— — —

GDP — Q2 | Prices

The pandemic has been a disinflationary shock to the economy. As measured by the GDP deflator, economy-wide inflation fell by 0.6% in Q2, slowing the annual pace from 1.7% to a 4-year low of 0.4%. The impact from the terms of trade was broadly neutral in the quarter. Adjusting for the terms of trade outcome, the gross national expenditure deflator reported a 0.7% decline in price levels in the June quarter to reduce the pace of growth through the year to 0.9% from 2.0%.

The closest proxy in the national accounts to the Consumer Price Index (CPI) is the household consumption deflator but it differs in that it accounts for dynamic shifts in spending patterns nationwide rather than the fixed basket capital city-based methodology in the CPI. The household consumption deflator declined by 0.8% in Q2 — its largest quarterly fall in more than half a century — reflecting a very sharp fall in petrol prices and a range of other cost-saving measures announced by governments and by the private sector, such as private health insurers delaying premium increases. As a result, the annual pace dropped down to 0.5% from 1.9%. By comparison, the CPI (seasonally adjusted) contracted by a much larger 2.0% in Q2 to be down by 0.5% through the year, with the ABS explaining that this was due to a different treatment within the national accounts around the Federal Government's policy decision to make child care service free during the shutdown.

The pandemic has been a disinflationary shock to the economy. As measured by the GDP deflator, economy-wide inflation fell by 0.6% in Q2, slowing the annual pace from 1.7% to a 4-year low of 0.4%. The impact from the terms of trade was broadly neutral in the quarter. Adjusting for the terms of trade outcome, the gross national expenditure deflator reported a 0.7% decline in price levels in the June quarter to reduce the pace of growth through the year to 0.9% from 2.0%.

— — —

GDP — Q2 | Productivity

The disruption caused by the shutdown and ongoing restrictions on activity led to hours worked across the domestic economy collapsing by 9.8% in the June quarter (-10.0%yr), coming after a 0.9% fall in Q1 (-0.4%yr) as the pandemic emerged in late March. Over the first half of 2020, hours worked fell by 10.6%. The disruptions were even more severe in the market sector (excludes government sector), with hours worked plunging by 12.2% (-13.3%yr) and by -13.5% over the first half.

As the decline in total hours worked (-9.8%) was larger than the decline in economic output (-7.0%), that mechanically led to a strong rise in GDP per hour worked (+3.2ppts to 4.2%Y/Y). GDP per capita fell by 7.2% in Q2 to be down by 7.4% over the year. Given the severity of the economic shock and the very significant shifts that have occurred in terms of how businesses operate, it is clearly not a time to be making judgments around productivity.

— — —

GDP — Q2 | States

State demand was down very sharply across the nation in the June quarter, though divergence will come through in Q3 to reflect the subsequent reversal of Victoria's reopening as the other states progressed their recoveries.

State demand was down very sharply across the nation in the June quarter, though divergence will come through in Q3 to reflect the subsequent reversal of Victoria's reopening as the other states progressed their recoveries.

Unsurprisingly, the contractions in Q2 were most severe in the two most populous states of New South Wales (-8.6%) and Victoria (-8.5%), reflecting the hit to household spending (-13.3% in NSW, -13.7% in VIC). Both states also recorded accelerated weakness in business investment as economic uncertainty weighed.

Household consumption also led the way down across the other states and declined by similar magnitudes in Queensland (-9.6%), South Australia (-9.9%) but was more severe in Western Australia (-10.6%) and Tasmania (-12.5%).

Household consumption also led the way down across the other states and declined by similar magnitudes in Queensland (-9.6%), South Australia (-9.9%) but was more severe in Western Australia (-10.6%) and Tasmania (-12.5%).