Following a sharp loss of momentum in the second half of 2018, the Australian economy eased further over the first half of 2019. On a seasonally adjusted basis, real GDP growth was 0.5% in the June quarter, printing in line with the consensus forecast, while the annual pace slowed from 1.8% to 1.4% — its slowest since Q3 2009 to around half the nation's trend rate of output growth.

Uncertainty was a key theme in the June quarter, with headwinds from offshore intensifying due to a deteriorating global economic outlook that is driven by a slowdown in manufacturing in response to escalating US-China trade disputes and geopolitical tensions in Europe. Domestically, uncertainty over government policy was prevalent in the lead up to May's federal election, while the Reserve Bank of Australia (RBA) recommenced its easing cycle by lowering the cash rate for the first time since 2016 due to softening labour market conditions and below-target inflation.

In the June quarter, the key dynamic in the domestic economy was the contrast in private and public sector demand. Demand in the private sector contracted by 0.1% in Q2 to be down by 0.3% over the year — its weakest since the GFC — which has been weighed by slowing household consumption in response to low income growth and weak housing market conditions, a downturn in residential construction activity and soft business investment. However, robust growth in public demand remains in train rising by 1.5% in Q2 and by 5.2% through the year, supported by healthcare spending and infrastructure investment.

Uncertainty was a key theme in the June quarter, with headwinds from offshore intensifying due to a deteriorating global economic outlook that is driven by a slowdown in manufacturing in response to escalating US-China trade disputes and geopolitical tensions in Europe. Domestically, uncertainty over government policy was prevalent in the lead up to May's federal election, while the Reserve Bank of Australia (RBA) recommenced its easing cycle by lowering the cash rate for the first time since 2016 due to softening labour market conditions and below-target inflation.

In the June quarter, the key dynamic in the domestic economy was the contrast in private and public sector demand. Demand in the private sector contracted by 0.1% in Q2 to be down by 0.3% over the year — its weakest since the GFC — which has been weighed by slowing household consumption in response to low income growth and weak housing market conditions, a downturn in residential construction activity and soft business investment. However, robust growth in public demand remains in train rising by 1.5% in Q2 and by 5.2% through the year, supported by healthcare spending and infrastructure investment.

— — —

GDP — Q2 | Expenditure: GDP (E) +0.4%q/q, +1.5%Y/Y

Household consumption (+0.4%q/q, +1.4%Y/Y) — Growth in household consumption was 0.4% in Q2, with the annual pace slowing to a 6-year low at 1.4%. Consumption spending has been soft for 4 consecutive quarters with the profile being; 0.3% (Q3 '18), 0.4% (Q4 '18), 0.3% (Q1 '19) and 0.4% (Q2 '19). *(click on the charts to expand)

The detailed breakdown of spending was fairly even in Q2, with discretionary up by 0.3% compared to a 0.4% lift from non-discretionary, though over the past year discretionary spending at 0.6% lags well behind growth in non-discretionary at 1.9%. Notable in Q2 were sizeable declines in spending on vehicles (-3.0%), tobacco (-0.9%) and utilities (-0.8%), while the increases were led by cafes and restaurants (+0.9%) and clothing and footwear (+0.7%).

Slow income growth remains an enduring headwind for the household sector, which reflects a labour market with an elevated level of spare capacity as well as weakness in productivity. Real growth in household disposable income declined by 0.3% in Q2 with the annual pace slowing from 1.0% to 0.5%. Given that real spending was up by 0.4% in the quarter against a decline in income, this led to a fall in the household saving ratio from 3.0% to 2.3% to be at its lowest since Q4 2007. This points to risks that the stimulatory impact from the RBA's June and July rate cuts and the increased tax offset for low-and middle-income earners may be dampened by households looking to lift saving by lowering consumption.

Dwelling investment (-4.4%q/q, -9.1%Y/Y) — The downturn in the residential construction cycle intensified with activity declining by 4.4% in Q2 — its weakest quarter in 6 years — and by -9.1% over the year, which is its sharpest rate of contraction in 7 years. Activity in new dwelling construction fell to its weakest since the GST-induced slowdown back in 2000, with a 5.9% contraction in Q2 to be down by 10.9% across the year. Alteration work fell by 1.4% in Q2 — its third consecutive quarterly decline — and has fallen by 5.6% in annual terms. Overall, the weakness in residential construction activity reflects the sharp deterioration in dwelling approvals over the past year, with the pipeline of work to be done now coming down in most states.

Business investment (-0.4%q/q, -1.6%Y/Y) — Underlying business investment was weak over the first half of 2019, with a 0.4% contraction in Q2 after a flat Q1, while the 1.6% annual decline was unchanged from Q1. Uncertainty over the global economic outlook and the policy framework in the lead up to the Australian federal election in May appear to have been significant headwinds for firms. The 0.4% decline in Q2 was centred on weakness in non-dwelling construction, with spending on new buildings (-5.0%q/q, -3.8%Y/Y) and engineering (-4.7%q/q, -14.8%Y/Y), the latter indicative of the nearing completion of major projects in the resources sector. The detail was much more constructive elsewhere in Q2; equipment and machinery +3.2% (+5.2%Y/Y), intellectual property products +2.9% (+7.3%Y/Y) and cultivated biological resources +4.1% (-9.0%Y/Y). The ABS's recent capital expenditure survey pointed to rising investment intentions from both the non-mining and mining sectors in 2019/20, though caution around this outlook appears warranted.

Public demand (+1.5%q/q, +5.2%Y/Y) — Strong growth in public demand continues and has been the leading contributor to activity over the past year. This has been supported by spending on health and aged care services and infrastructure investment for transport and electricity-related projects. However, the profile in Q2 was mixed with consumption spending up by 2.7% and underlying investment down by 3.2%.

Net exports (+0.6ppt in Q2, +1.2ppt yr) — At 0.6ppt in Q2, net exports made their strongest contribution to growth since the March quarter of 2018, and follows on from a 0.4ppt contribution in Q1. Export volumes lifted by 1.4% in Q2, with broad-based support from resources, after a 1.9% rise in Q1. Meanwhile, import volumes declined by 1.3% in Q2 after a soft outcome of -0.2% in Q1, which reflects weak domestic demand conditions and a lower Australian dollar.

— — —

GDP — Q2 | Incomes: GDP (I) +0.6%q/q, +1.4%Y/Y

The real GDP income estimate lifted by 0.6% in the June quarter, which was stronger than both the expenditure and production estimates, while the annual pace remained at its equal lowest since Q3 2009 at 1.4%.

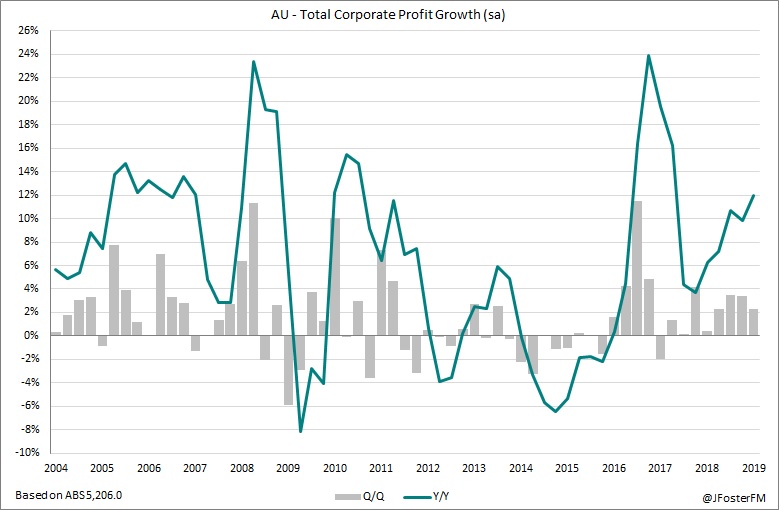

In nominal terms, Australian GDP growth was 1.2% in Q2 to be up by 5.4% through the year. Growth has been robust in each of the past 6 quarters and has driven the annual pace off its recent low of 3.8% in Q4 2017. The key dynamic has been escalating commodity prices and this has generated a tailwind for national income. The terms of trade increased by a further 1.5% in the June quarter, though this was much lower than the increases of 3.0% and 3.1% in the previous two quarters. In year-on-year terms, growth in the terms of trade lifted from 6.0% to 8.9% — its fastest rate of expansion since Q3 2017.

— — —

GDP — Q2 | Production: GDP (P) +0.5%q/q, +1.5%Y/Y

The production estimate for GDP in Q2 was 0.5%, which was in the middle of the expenditure (0.4%) and income (0.6%) estimates. The annual pace continues to slow, moving down from 1.8% to 1.5% to its weakest since Q3 2009.

There were 7 industries that weighed on output in Q2 compared to 4 in Q1. These industries were; agriculture (-2.1%), construction (-1.4%), manufacturing (-1.4%), wholesale trade (-1.4%), utilities (-0.3%), transport (-0.3%), and arts and recreation (-0.1%). Drought conditions continue to heavily impact output from the agriculture sector and the construction industry is weighed by weakness in residential and commercial building.

The health sector led output over the past year at 7.9%, driven by public spending associated with the rollout of initiatives such as the NDIS and PBS and aged care services. Output in Q2 was strongest in the Mining sector (+3.4%) and second overall for the year at 6.2%, due largely to the ramp up in LNG production as completed projects come on line. The industry-by-industry breakdown for Q2 and for the year is shown in the chart, below.

There were 7 industries that weighed on output in Q2 compared to 4 in Q1. These industries were; agriculture (-2.1%), construction (-1.4%), manufacturing (-1.4%), wholesale trade (-1.4%), utilities (-0.3%), transport (-0.3%), and arts and recreation (-0.1%). Drought conditions continue to heavily impact output from the agriculture sector and the construction industry is weighed by weakness in residential and commercial building.

The health sector led output over the past year at 7.9%, driven by public spending associated with the rollout of initiatives such as the NDIS and PBS and aged care services. Output in Q2 was strongest in the Mining sector (+3.4%) and second overall for the year at 6.2%, due largely to the ramp up in LNG production as completed projects come on line. The industry-by-industry breakdown for Q2 and for the year is shown in the chart, below.

— — —

GDP — Q2 | Prices

— — —

GDP — Q2 | Productivity

National productivity growth remains mired in a period of weakness and is a strong structural headwind for wages growth. However, there was a slight improvement this quarter. Growth in total hours worked in the quarter was 0.1% and was exceeded by output growth of 0.5%, thus real GDP per hour worked expanded by 0.4% in Q2 — its best result in 5 quarters. However, it remains in contraction over the year, though the rate of decline was cut from -1.2% to -0.2%.

In the market sector, which excludes the public sector, GDP per hour worked was flat in Q2 after consecutive quarterly declines of 0.3%, while the annual pace remains very weak at -0.6% but improved marginally from -0.8%. On this basis, productivity remains at around an 8-year low. Real GDP per capita stalled in Q2 after rising by 0.1% in Q1 and followed contractions of 0.1% and 0.2% in the second half of 2018. In annual terms, real GDP per capita fell by 0.2% to be at its weakest since the GFC.

GDP — Q2 | States

Demand in Victoria increased by 0.5% in Q2, though a base effect resulted in the annual pace slowing to 1.9% from 2.5%, which is its softest since Q3 2014. Annual growth in household consumption has slowed to a 6-year low at 1.9% in line with softening labour market conditions over the first half of the year. After a weak second half of 2018, the downturn in residential construction intensified over the first half of this year with declines in both construction and alterations. The public sector remains supportive of state demand, and despite a weak period over the last year, investment is likely to pick up given the pipeline of work to be done around infrastructure, which will have flow-on benefits for the private sector.

In the other states, demand in Queensland stalled in Q2 slowing the annual pace to just 0.4%. Household consumption continues to be subdued, though Q2 saw a decent rise of 0.7% to be up by 2.2% for the year. Business investment remains weak, particularly in the area of engineering construction. In South Australia, demand contracted by 0.2% in Q2 — as was the case in Q1 — with annual growth decelerating from 1.6% to 0.4%. The factors driving this slowdown have been weakening household consumption, a rollover in the residential construction cycle, and declining business investment. Demand in Western Australia lifted by 0.8% in Q2 — its strongest quarter since Q3 2017 — though it still remained down on a year earlier at -0.1% despite improving from -1.6%. The quarterly result was boosted by equipment spending, but household consumption is subdued and residential construction is in the midst of a sharp downturn. State demand in Tasmania was 0.3% in Q2, and while the annual pace slowed from 4.1% to 3.1% it remained the strongest in the nation. This has been boosted by public spending, which has helped to offset slowing household consumption, residential construction and business investment.

In the other states, demand in Queensland stalled in Q2 slowing the annual pace to just 0.4%. Household consumption continues to be subdued, though Q2 saw a decent rise of 0.7% to be up by 2.2% for the year. Business investment remains weak, particularly in the area of engineering construction. In South Australia, demand contracted by 0.2% in Q2 — as was the case in Q1 — with annual growth decelerating from 1.6% to 0.4%. The factors driving this slowdown have been weakening household consumption, a rollover in the residential construction cycle, and declining business investment. Demand in Western Australia lifted by 0.8% in Q2 — its strongest quarter since Q3 2017 — though it still remained down on a year earlier at -0.1% despite improving from -1.6%. The quarterly result was boosted by equipment spending, but household consumption is subdued and residential construction is in the midst of a sharp downturn. State demand in Tasmania was 0.3% in Q2, and while the annual pace slowed from 4.1% to 3.1% it remained the strongest in the nation. This has been boosted by public spending, which has helped to offset slowing household consumption, residential construction and business investment.