Housing Finance — May | By the numbers

- Housing finance approvals to owner-occupiers (excluding refinancing) eased by 0.1% to 30,820 -- an upside surprise relative to the median expectation for a 1.0% fall (prior rev: -0.9% from -1.1%). Approvals declined by 15.0% year-on-year, accelerating from a 13.5% fall over the year to April.

- The total value of housing finance commitments (excluding refinancing) fell by 2.4% in the month to $A16.5bn (prior rev: 0.0% from +0.2%), with the annual decline steepening to -20.9% from -17.6%.

Housing Finance — May | The details

Lending commitments declined by 2.4% in aggregate excluding refinancing in May to $16.5bn, with the owner-occupier segment falling by 2.7% to $12.2bn (-18.1%Y/Y) and investor lending sliding by 1.7% to $4.3bn (-27.8%Y/Y). Refinancing commitments lifted by 0.5% in the month (-8.4%Y/Y), with increases for both owner-occupiers (+0.5%m/m, -7.0%Y/Y) and investors (+0.4%m/m, -11.6%Y/Y). Lending for alterations to existing properties in the owner-occupier segment declined by 1.6% for the month to $269.6m, which saw the annual pace slow from -11.8% to -14.6%.

Total loan approvals to owner-occupiers were almost flat in May (-0.1%), though the decline over the year extended to -15.0% from -13.5%. Approvals to purchase existing dwellings pulled back by 0.8% (-16.0%Y/Y). Construction-related approvals were up by 2.3% in the month (-11.7%Y/Y), which was centred around a 3.5% rise for loans to fund new construction (-4.6%Y/Y), as approvals to purchase newly constructed dwellings eased by 0.6% (-25.8%Y/Y). The ABS does not produce approval estimates for the investor segment.

The state details across all borrower types in May are broken down in the table, below.

Despite mixed results in May, the chart (below) confirms that approvals across the nation remain on a downward trajectory, driven largely by New South Wales, Victoria, and Queensland.

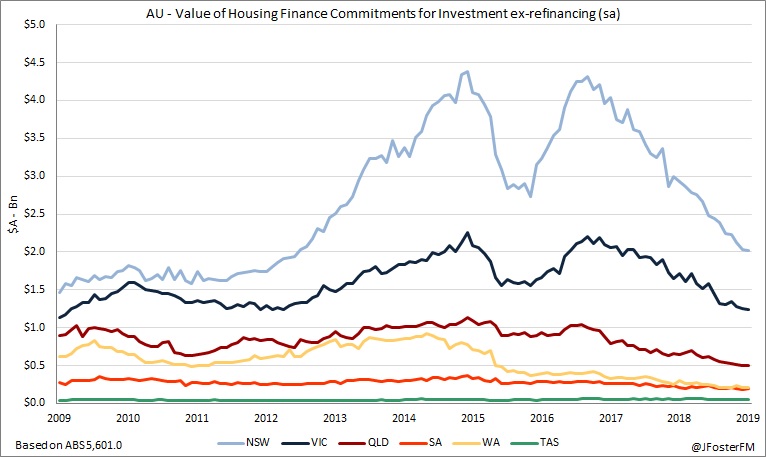

Moreover, the downturn in investor activity showed no sign of slowing in May's release.

Housing Finance — May | Insights

This series remains pre-dated by the recent federal election outcome, the RBA's June and July rate cuts, as well as the decision by regulator APRA to ease its guidance around lending criteria applied by the banks. More timely indicators in the form of price and auction clearance data suggest some early signs of stabilisation in the Sydney and Melbourne markets, though volumes remain low.