The US Federal Reserve's (Fed) latest meeting headlined developments this week by marking a notably dovish shift in tone (see here). While still retaining a constructive baseline view for the US economic outlook, "increased uncertainties and muted inflationary pressures" prompted the Committee to remove its "patient" guidance used throughout 2019 to a stance where it will now "act as appropriate to sustain the (economic) expansion, with a strong labour market and inflation near its symmetric 2 percent objective".

Underlining this shift, 8 of 19 Committee members expected rates to be cut this year, with 7 of those projecting 50 basis points of easing and the remaining voter seeing one rate cut. In sum, that was one shy from seeing the median projection for 2019 lowered from the present 2.25-2.5% setting (shown as our chart of the week, below), though the risks are to the downside with Fed Chair Powell saying in the post-meeting press conference that "a number of others see the case (for rate cuts) is strengthened". For 2020, the median projection implies the Committee will ease -- a complete reversal from just 3 months ago when the signal was for a rate hike.

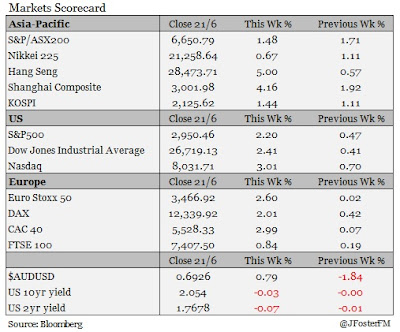

Chart of the week

There is now also an increased willingness from policymakers to support the euro area economy as outlined by European Central Bank (ECB) President Draghi during an address at its annual forum in Sintra. The message from the ECB's meeting 2 weeks ago was that the Governing Council was "determined to act in case of adverse contingencies", though in a surprise to markets that outlook was strengthened by President Draghi on Tuesday, highlighting that "additional stimulus will be required" unless they observe an improvement in the data flow. As President Draghi outlined, all stimulus options are under firm consideration including restarting net asset purchases and interest rate cuts.

The Bank of England has yet to join the dovish shift, with the decision statement from its latest meeting this week continuing with its expectation for "gradual" and "limited" tightening in monetary policy. The Bank's assessment is that in response to tight labour market conditions and strength in wages growth, inflationary pressures will begin to emerge. However, that view remains conditioned on an orderly Brexit transition, which in itself is far from certain.

Rounding out the week from abroad, the Bank of Japan maintained its policy stance but is clearly alert to the downside risks posed to the domestic economy -- most notably in its export sector -- by the escalation in global trade tensions (and by further strengthening in the Yen). Governor Kuroda said the Bank's Policy Board would "consider expanding stimulus without hesitation", which could include expanded asset purchases and lower interest rates.

Rounding out the week from abroad, the Bank of Japan maintained its policy stance but is clearly alert to the downside risks posed to the domestic economy -- most notably in its export sector -- by the escalation in global trade tensions (and by further strengthening in the Yen). Governor Kuroda said the Bank's Policy Board would "consider expanding stimulus without hesitation", which could include expanded asset purchases and lower interest rates.

—

In keeping with the global theme, it was the Reserve Bank of Australia (RBA) that gained most of the focus domestically this week. June's meeting minutes conveyed that the Board's outlook for the Australian economy "remained reasonable" supported by an expected lift in household income, public investment and resources exports. The minutes also highlighted that the decision to cut the cash rate by 25 basis points earlier this month was prompted by a revised assessment of the labour market, now seeing that a much lower unemployment rate of around 4.5% can be sustained without generating inflationary concerns. Given that the unemployment rate lifted to 5.2% in April (and remained unchanged in May) members concluded that "it was more likely than not that a further easing in monetary policy would be appropriate in the period ahead".

That could occur as early as the next meeting, with markets increasing the probability for a rate cut on July 2 to around 75% from around 50% following a speech from RBA Governor Lowe in Adelaide on Thursday. Therein, more insight was provided on the various perspectives taken by the Bank to assess the extent of spare capacity in the labour market. Notable insights were that the labour supply in Australia is highly flexible to increases in demand, while wages growth is running well below a pace consistent with inflation returning to the Bank's 2-3% target range.

With the RBA now setting its sights on driving the unemployment rate lower, Governor Lowe signaled a clear preparedness for additional easing by noting that it would be "unrealistic to expect that lowering interest rates by ¼ of a percentage point will materially shift the path we look to be on". Strengthening that view, the Governor saw no sign from May's labour market data or Q1's national accounts that progress on reducing excess capacity was being made and thus "the possibility of lower interest rates remains on the table". Current expectations between financial markets and economists are for the cash rate to fall to 0.75% by year's end.