Business Indicators — Q3 | By the numbers

- Inventories were flat in Q3 (0.0%), below the market expectation for an increase of 0.4% (prior rev +0.7% from +0.6%)

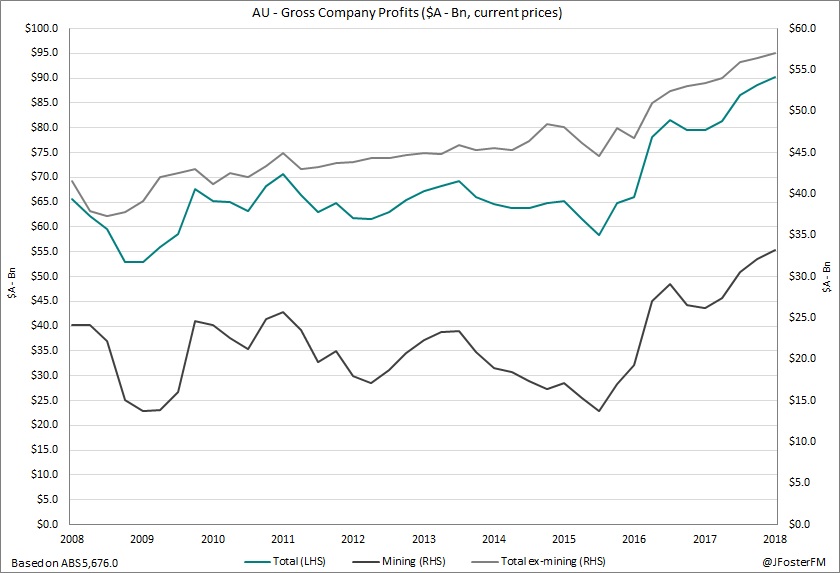

- Company gross operating profits lifted by 1.9% in Q3 to $A90.221bn, well short of the market forecast for +2.8% (prior rev +2.4% from +2.0%). Annual growth in profits increased to 13.5% from 11.3%.

- Growth in wages and salaries paid posted a 0.9% rise in the quarter to $A138.28bn (prior rev +1.2%), which saw annual growth ease to 4.3% from 4.5%

Business Indicators — Q3 | The details

The inventories component measures the change in the value non-farm inventories held by firms in the quarter. A 'build' in inventories can point to an expectation of firms for increased demand in the future. Overall, the change in inventories was flat in Q3. The detail was soft with declines in the quarter for; mining -0.9%, manufacturing -0.4%, utilities -2.4% and wholesale trade -0.7%. Retail (+2.3%) was the only sector that posted an increase in Q3. Total inventories have lifted only modestly (+1.6%) across the year, unchanged from the pace for the year-ending Q2 after allowing for revisions.

On company profits, the total increase of 1.9% in Q3 was the softest quarterly outcome in a year. Annually, though, profits have increased by 13.5% from the 11.3% pace in Q2. This component flows into estimates of profitability for non-financial corporations within the National Accounts.

Breaking this down further, profitability continues to be led by the mining sector, which posted a 3.4% rise in the quarter to be running at an annual pace of 27.1%. Surging prices for key export commodities have driven profitability in the sector, which should also provide a Terms of Trade boost in the National Accounts.

Profitability in the non-mining sector has been more modest, with a 1% rise in Q3 and a slight increase in annual terms to 6.8%. Across the sectors, profitability increased in the quarter for; utilities (+7.0%), construction (+9.7%), accommodation and food services (+13.5%), media and telecommunications (+3%), financial and insurance services (+1.3%), real estate services (+3.1%), administration (+4.7%) and recreation (+9.7%). There were declines in the quarter for; manufacturing (-5.1%), wholesale trade (-1.1%), retail (-2%), transport (-2.7%), professional services (-1%) and 'other' services (-8.1%).

Lastly, the wages and salaries component is used as the primary estimate for the key Compensation of Employees figure in the National Accounts. This figure is effectively the nation's total wages bill for the quarter and therefore reflects growth in employment and hours worked. For Q3, that mix yielded a rise of 0.9% — moderating from 1.2% last quarter. The quarterly figure has averaged growth of 1% over the past year. This saw the annual pace ease to 4.3% from 4.5%.

Business Indicators — Q3 | Insights

This provides another soft lead looking towards the quarterly GDP growth figure for Q3 following a similar outcome from last week's Construction Work Done data, though the equipment data from the Capital Expenditure data was positive. In Q2, inventories made a flat contribution to the quarterly GDP growth figure but will be a drag in Q3 — potentially by around as much as -0.3ppt. On incomes, rising company profitability has been supported by above-trend growth and positive trading conditions, and wages have been driven by strong employment growth.