In the US, the focus was on the early stages of the corporate reporting season. Last week's scrutiny over corporate valuations makes this a particularly important period as markets look for confirmation that earnings growth can sustain elevated valuations. Overall, the headline detail appeared generally positive, highlighted by Netflix posting above-consensus earnings following strong subscription growth. The news was also positive in the financial sector, with better-than-expected results from the major banks; JP Morgan Chase, Morgan Stanley, Goldman Sachs', Wells Fargo and Citi, although Bank of America Merril Lynch disappointed on loan growth. Outside of financials, the main disappointments were from IBM and Walmart.

For Australia, the strong results posted by US banks had helped to put a floor under the heavy declines in the financial sector from last week, although the recovery was modest in that context. Across the week, the benchmark ASX200 index posted a solid rise, which was supported by the consumer sectors.

More broadly, the major indices in Europe mostly saw modest weekly gains after declining sharply by more than 4% last week. In Asia, against the trend of less volatile global markets, China's major indices fell heavily again this week — despite a rebound on Friday — weighed by broader concerns over the growth outlook and financial stability.

—

In Australia, the focus this week was on the labour market. Firstly, the Reserve Bank of Australia's (RBA) Deputy Governor Guy Debelle delivered a speech titled 'The State of the Labour Market', where the commentary continued to reflect the RBA's upbeat assessment of conditions.

In summary, the RBA expects employment growth to remain above average and run ahead of growth in the working-age population. Combined with its forecasts for above trend economic growth, it continues to expect a gradual erosion in 'spare capacity' (unemployed and underemployed workers) and, in turn, a gradual rise in wages growth, which would ultimately lift inflationary pressures.

In summary, the RBA expects employment growth to remain above average and run ahead of growth in the working-age population. Combined with its forecasts for above trend economic growth, it continues to expect a gradual erosion in 'spare capacity' (unemployed and underemployed workers) and, in turn, a gradual rise in wages growth, which would ultimately lift inflationary pressures.

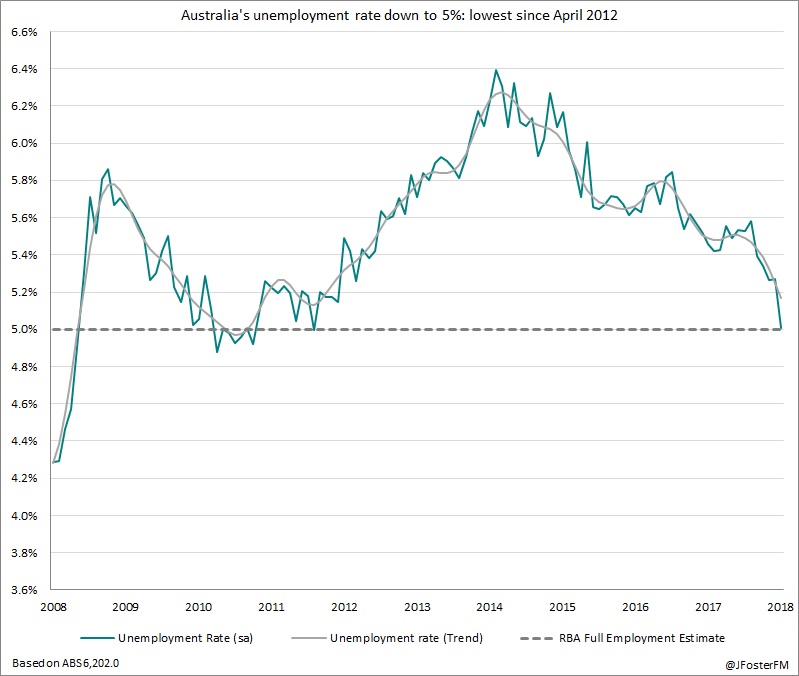

Secondly, Australia's latest employment data for the month of September were released during the week. While only 5,600 jobs were added in the month, below an expected addition of 15,000, the nation's unemployment rate fell to 5% on a seasonally adjusted basis — its lowest level in more than six years and therefore is our chart of the week.

Chart of the Week

Historically, the RBA has estimated Australia's rate of full employment to be around 5%. In technical terms, this is referred to as the non-accelerating inflation rate of unemployment (NAIRU), which is the level of unemployment where wage and inflationary pressures generally remain stable.

However, as outlined in our review of September's Labour Force Survey, the sharp fall in the unemployment rate is not likely to portend a faster rise in wages growth in the near term. Furthermore, recent global experiences would suggest that unemployment rates have had to decline well below previously estimated NAIRU's to stimulate wage pressures, so this could also be the case for Australia.

However, as outlined in our review of September's Labour Force Survey, the sharp fall in the unemployment rate is not likely to portend a faster rise in wages growth in the near term. Furthermore, recent global experiences would suggest that unemployment rates have had to decline well below previously estimated NAIRU's to stimulate wage pressures, so this could also be the case for Australia.

The main event during the week from a global-macro perspective were the minutes from the US Federal Reserve's meeting in September, where it increased its benchmark interest rate by 25 basis points to a target of 2-2.25%.

The key point from these minutes was that the Fed sees the need for further interest rate increases given strong economic growth and a tight labour market. Of note, Fed members had discussed the possibility of rates being increased temporarily to a 'modestly restrictive' level to reduce the risk of inflation running above its 2% target and to prevent imbalances to financial stability from building up. While support for this stance was not unanimous without clearer signs of an overrun in inflation, it appears that the Fed is set to maintain its path for tightening, which as implied by its 'dot plot' points to one further increase in December, followed by three increases in 2019.

The key point from these minutes was that the Fed sees the need for further interest rate increases given strong economic growth and a tight labour market. Of note, Fed members had discussed the possibility of rates being increased temporarily to a 'modestly restrictive' level to reduce the risk of inflation running above its 2% target and to prevent imbalances to financial stability from building up. While support for this stance was not unanimous without clearer signs of an overrun in inflation, it appears that the Fed is set to maintain its path for tightening, which as implied by its 'dot plot' points to one further increase in December, followed by three increases in 2019.

In Europe, last week's optimism that a Brexit deal may be imminent seemed to fray given renewed uncertainty over negotiations regarding the Ireland-Northern Ireland border issue. UK Prime Minister Theresa May also said she would consider the possibility of extending the 'transition period' for "a matter of months" after Britain exits the European Union (EU) in March next year, but that would still need to be supported by the parliament.

The greater risk to markets from Europe are the tensions between the EU and Italy over its budget. Italy released its budgetary plans for 2019, which would increase its deficit to 2.4% of GDP — a level 3-times above the 0.8% target mandated by the EU and agreed to by the previous government. European Central Bank President Mario Draghi warned that contravention of the target would "carry a high price" for the other eurozone economies.

Rounding out the global risk factors, China's GDP growth for the September quarter slowed to an annual pace of 6.5%, which was a touch softer than expected by markets (6.6%). Policymakers in China face a delicate balance between implementing stimulus measures to ward off moderating economic growth, with the impact of trade tensions yet to be fully reflected in the data, while at the same time managing risks to financial stability from earlier concerns over the quality of lending, particularly from the non-bank sector.