Hawkish messaging from central banks around the need to take rates higher appeared to be taken on board as the bullish sentiment running through markets lost momentum. Many equity markets saw their first weekly declines in 2023. Bond yields steepened, notably so in Australia following more aggressive forward rate guidance from the RBA. But markets were largely in a holding pattern ahead of next week's US CPI data; the headline rate is expected to ease from 6.5% to 6.2% in January and from 5.7% to 5.4% on the core rate.

RBA steps up hawkish stance

The RBA Board delivered a hawkish hike of 25bps to 3.35% at its first meeting in 2023 (see here). Strengthened guidance in Governor Lowe's meeting statement for "further increases" in rates saw markets reprice the peak cash rate to around 4% and pushed back the timing for a pause. The Board has taken on a more hawkish leaning as underlying inflation pressures in Australia surprised to the upside in the December quarter.

As a result, the RBA's February Statement on Monetary Policy (SoMP) projects a slower decline in inflation in the year ahead. Headline CPI is anticipated to fall from 7.8% currently to 4.8% (from 4.7% previously) but it was the slower progress in trimmed mean inflation at 6.9% to 4.3% by year-end (from 3.8%) that has the RBA's attention. Alongside this, the RBA's liaison program has picked up that the strong labour market is supporting a faster pace of wages growth; the forecast for 2023 projects a rise to 4.2%, up from 3.9% earlier expected. Inflation pressures are forecast to ease at a slightly faster pace through 2024 ahead coming back to the top of the target band in mid-2025.

The growth forecasts at 1.6% in 2023 and 2024 were essentially unchanged and suggest the RBA's central scenario is that it can "keep the economy on an even keel" as it brings down inflation. But with rates set to press higher, the SoMP notes the path to achieving this soft landing for the economy "remains narrow". There are major uncertainties around the consumer and how spending patterns will hold up amid the crosscurrent from cost-of-living pressures and rising interest rates while at the same time, the labour market is supporting income and the stock of savings built up over the pandemic remains large on aggregate.

On the data front this week, retail sales volumes declined in the December quarter on a combination of higher prices and spending continuing to rotate to services post the pandemic (see here). Trade data reported the trade surplus elevated to $12.2bn and widened substantially over the final quarter of the year, which looks likely to drive a sizeable positive contribution to GDP growth from net exports (see here).

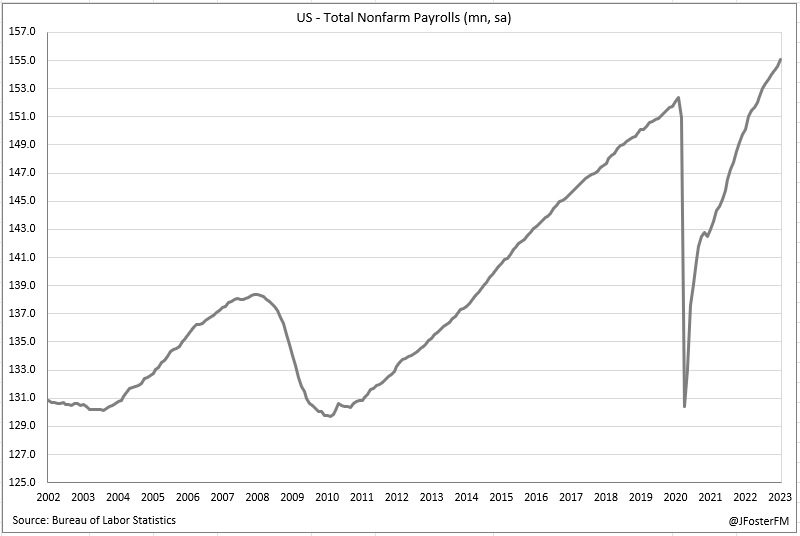

US payrolls report continues to reverberate

January's very strong labour market report saw Federal Reserve officials pushing a hawkish line, reiterating the message from last week's FOMC meeting that rates had further to rise. Fed Chair Powell told an audience at the Economic Club of Washington that while a "disinflationary process" is underway, lowering inflation to the target would likely "take quite a bit of time, and is not going to be smooth". Chair Powell said the labour market was "extraordinarily strong" and meant that a persistence of services-related inflation could elongate the process. Other Fed officials including Waller, Cook, Williams and Kashkari all said during their remarks this week that further rate increases were on the table.

UK growth stalls

Growth in the UK economy stalled in the December quarter and slowed sharply over the year (0.4%) as the post-pandemic rebound was cycled and cost-of-living pressures impacted spending. Pay disputes affecting the transport and health sectors also appear to have been a factor that hampered activity in the most recent quarter. Governor Bailey told members of the Treasury Committee that the Bank of England's latest rate hike came in response to upside risks to inflation feeding through from wage-setting processes.

In Europe, the delayed German inflation print for January was the highlight of the week. Headline inflation lifted a touch to 8.7%yr (from 8.6%) but this was slightly below expectations for 8.9%. However, the EU-harmonised measure showed a softening from 9.6% to 9.2% in December. ECB officials followed up last week's meeting with hawkish comments. Vice President de Guindos said the ECB had observed signs that its tightening cycle was taking effect on financing conditions but that the Governing Council was likely to raise rates by a further 50bps at the March meeting.