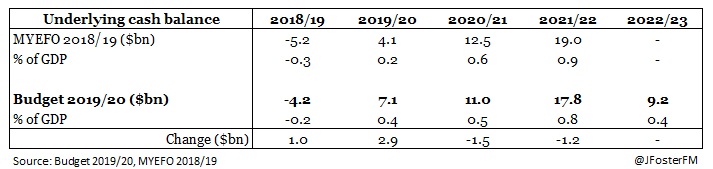

Overall, the profile of the budget has been revised modestly higher by $1.3bn over the 4 years out to 2021/22 compared with the forecasts from MYEFO. That reflects improved outcomes in the near term in 2018/19 and 2019/20, though the surpluses projected for the out years in 2020/21 and 2021/22 have been lowered.

The details are now; 2018/19 a deficit of -$4.2bn ($1.0bn improvement), 2019/20 a surplus of $7.1bn ($2.9bn improvement), 2020/21 a surplus of $11.0bn ($1.5bn downgrade) and 2021/22 a surplus of $17.8bn ($1.2bn downgrade). The variations are shown in the table, below (click to expand).

Government net debt is forecast to lift from 18.2% to 19.2% of GDP by the end of the 2018/19 financial year. The trajectory is then expected to improve in 2019/20 to 18.0% of GDP ahead of further moderation over the out years to an eventual 14.4% of GDP in 2022/23 (see table, below).

Since MYEFO — Budget 2019/20

Key to Budget 2019/20 is that it starts on an improved position relative to expectations from MYEFO. Since December, elevated prices for the nation's key commodity exports have held, delivering a sizeable boost to company tax receipts, particularly from the mining sector. This will continue to benefit the Government's fiscal position through 2019/20, due to the timing delay between the accrual of profit and when companies pay tax. Meanwhile, forecast expenditure has been lowered, mainly to reflect reduced GST distributions to the states in response to a weaker outlook for residential construction and household consumption, and a slower-than-anticipated transition of participants into the National Disability Insurance Scheme.

For 2018/19, the budget starts $4.0bn ahead of expectations from MYEFO and then by $5.7bn in 2019/20. The improvements then moderate to $1.4bn in 2020/21 and to $0.2bn in 2021/22. In total, this improves budget position by a total of $11.3bn over the four years out to 2021/22 (see table, below).

New Policy Measures — Budget 2019/20

Given this improved fiscal position, the Government has announced a series of new policy measures since MYEFO was tabled, of which the net impact presents a cost to the budget of $9.9bn over the coming 4 years. In detail, the new measures will have a net impact of $3.0bn in 2018/19, $2.7bn in 2019/20, $2.8bn in 2020/21 and $1.4bn in 2021/22. The projection for 2022/23 is for the net impact to accelerate to $3.4bn, in response to the Government's plan to raise the top threshold to the 19% tax bracket and increase the low income tax offset.

Budget 2019/20's new measures result in expenditure increasing by a total of $10.5bn over the coming 4 years. The headline new policy announcements include;

Revenue Measures (lowering government revenues)

Expense Measures (increasing goverment expenditure)

For 2018/19, the budget starts $4.0bn ahead of expectations from MYEFO and then by $5.7bn in 2019/20. The improvements then moderate to $1.4bn in 2020/21 and to $0.2bn in 2021/22. In total, this improves budget position by a total of $11.3bn over the four years out to 2021/22 (see table, below).

Given this improved fiscal position, the Government has announced a series of new policy measures since MYEFO was tabled, of which the net impact presents a cost to the budget of $9.9bn over the coming 4 years. In detail, the new measures will have a net impact of $3.0bn in 2018/19, $2.7bn in 2019/20, $2.8bn in 2020/21 and $1.4bn in 2021/22. The projection for 2022/23 is for the net impact to accelerate to $3.4bn, in response to the Government's plan to raise the top threshold to the 19% tax bracket and increase the low income tax offset.

Budget 2019/20's new measures result in expenditure increasing by a total of $10.5bn over the coming 4 years. The headline new policy announcements include;

Revenue Measures (lowering government revenues)

- "Lower taxes for hard-working Australians" (increasing the low and middle income tax offset base from $200 to $255 for incomes up to $37,000, which rises incrementally for incomes between $37,000 to $48,000, with the maximum offset lifting from $530 to $1,080 to be available for incomes between $48,000 to $90,000, before gradually phasing out to zero at $126,000): 2019/20 cost $0.8bn, 4yr cost $5.7bn

- Increasing instant asset write-offs (from $25,000 to $30,000) for small businesses and expanding access to now include medium-sized businesses: 2019/20 cost $0.2bn, 4yr cost $0.4bn

- Increases to the Medicare levy low-income thresholds: 2019/20 cost $0.1bn, 4yr cost $0.3bn

Expense Measures (increasing goverment expenditure)

- Infrastructure Investment Program — Urban Congestion Fund (next priorities): 2019/20 cost $0.4bn, 4yr cost $1.6bn

- Infrastructure Investment Program — Victorian Infrastructure Investments: 2019/20 cost $0.1bn, 4yr cost $1.2bn

- Medicare — Strengthening primary care: 2019/20 cost $0.1bn, 4yr cost $1.1bn

- Aged care — More Choices for a Longer Life: 2019/20 cost $0.1bn, 4yr cost $0.6bn

- Universal Access to Early Childhood Education — 2019/20 cost $0.1bn, 4yr cost $0.4bn

These measures are partly offset through savings made on the expense side, including from;

- Changing the Social Security Income Assesment Model — 2019/20 saving $0.0bn, 4yr saving $2.2bn

- Better Distribution of Medical Practitioners — 2019/20 saving $0.0bn, 4yr saving $0.3bn

- Extension and expansion of the ATO Tax Avoidance Taskforce on Large Corporates, Multinationals and High Wealth Individuals: 2019/20 increase $0.1bn, 4yr increase $3.6bn

Economic Forecasts — Budget 2019/20

The key economic forecasts the budget is based around include a downgrade to the outlook for the domestic economy in the near term. The real GDP growth forecast since MYEFO has been lowered to a below-potential rate of 2.25% in 2018/19 from the expectation for trend growth of 2.75% back in December. This lower starting point sees GDP growth improving in 2019/20, but only to trend (2.75%), whereas in MYEFO growth was anticipated to reach 3.0%.

The softer outlook comes mostly in response to an acknowledgment of slower growth in household consumption through the second half of 2018 and a deterioration in the forecast for residential construction activity, impacted by property price declines, weakening approvals, tight credit conditions and dampened buyer sentiment. However, household consumption growth is forecast to improve in 2019/20, driven by the expectation for solid labour market conditions to continue, in turn leading to a pick-up in wages growth. Based on the current data flow, the risks appear to the downside.

The Government anticipates the growth outlook to be supported by non-mining business investment, with a 4% rise in 2019/20 after being in decline for nearly 7 consecutive years, public demand associated with its rollout of infrastructure projects, and export growth through the LNG sector, tourism, and education.

The forecasts acknowledge a strengthening in the headwinds to the domestic economy from slowing momentum in the global economy. Global growth is now forecast to be 3.5% in 2019, 2020 and 2021, which is a slight downgrade compared with MYEFO. However, Treasury elected to retain forecast growth in the economies of the nation's major trading partners, including the US and China, at 4% in 2019, 2020 and 2021. A resolution to ongoing trade tensions is key to the global growth outlook.

MYEFO had set conservative forecasts for the prices of the nation's key commodities exports, with iron ore US$55/t, metallurgical coal US$120/t and thermal coal US$93/t (all quotes are Free on Board — FOB — prices). Since December, the spot iron ore price has run a little below US$90/t, while the metallurgical coal price averaged around US$200/t (FOB) across 2018, and the thermal coal price was also slightly stronger than anticipated. The upside surprise in commodities prices has delivered a sizeable lift to national income and is reflected through the Government's strengthened fiscal position.

This tailwind is expected to last for a little longer yet, with the terms of trade forecast to rise by 4% over 2018/19. However, that turns in 2019/20 where a decline of 5.25% is forecast ahead of a 4.75% slide in 2020/21. This reflects an expected fall in commodities prices by Q1 2020; iron ore to US$55/t (FOB) and metallurgical coal to US$150/t (FOB). National income, as measured by growth in nominal GDP, is forecast to rise by 5.0% in 2018/19 before moderating to 3.25% in 2019/20 and then lifting to 3.75% in 2020/21.

Market Implications — Budget 2019/20

Growth in the domestic economy slowed sharply over the second half of 2018 to a well-below trend pace of 2.3% through the year (see chart, below). Activity was reasonably strong in the first half of 2018, expanding by an annualised pace of around 4%, which then fell to a 1% annualised pace for the second half, as household consumption slowed in response to persistent weakness in wages growth and a decline in net worth driven by falling property and equity prices, while activity in the residential construction sector turned over. In addition, Reserve Bank of Australia (RBA) analysis has identified that growth in taxes paid by households has been stronger than usual recently and beyond what is typically associated with bracket creep. These factors point to the need for stimulus in the domestic economy.

Financial markets expect this stimulus to come from an RBA interest rate cut of 0.25% by August, with increasing anticipation for a follow-up cut by year-end. Budget 2019/20 offers fiscal stimulus through tax relief to low-and-middle-income earners, which plans to return $750m to households in the financial year. Whether that would offer more than a short-term impact and be sufficient to alleviate some of the headwinds facing the household sector are the key questions for policymakers, financial markets, and the electorate.

Link to Budget 2019/20 here