Tariff confusion became even more elevated this week, though the reaction across broad markets was fairly contained. The White House insists it will impose its liberation day tariffs one way or another despite being ruled invalid by the International Court of Trade. In a further twist, Trump announced on Friday that his sectoral tariffs on steel, which were not affected by the court's decision, would increase from 25% to 50%. Increased uncertainty as well as a potential reduction in Japanese bond issuance contributed to lower yields globally this week. Meanwhile, the USD rose off the back of the tariff court ruling but those gains were not sustained as an appeals court granted a stay on the decision.

US inflation data was encouraging as the Fed's preferred core PCE deflator came in at a soft 0.1%m/m in April to a 2.5%yr pace, down from a prior reading of 2.6%. But as highlighted in the minutes of the Federal Reserve's policy meeting from earlier this month, tariffs are expected to push up imported goods prices, with some concern that this will lead to spillover effects on inflation more broadly. On tariffs, April data showed the largest drop in monthly imports on record (19.8%), narrowing the trade deficit from $163bn to $88bn.

At next week's meeting, the ECB is expected to continue its easing cycle with another 25bps rate cut, lowering the depo rate to 2%. Trump said he will delay his threatened 50% tariff on European imports until July 9 (from June 1), but the growth outlook in the bloc is still under pressure. In spite of this, trade weighted euro remains around record highs, which together with a weaker growth outlook, is reducing inflationary risks and that should keep the ECB's hawks in the minority. At the Bank of England, Governor Bailey reaffirmed that the strategy of 'gradual and careful' rate cuts remains appropriate amid the uncertainty of trade tariffs on UK inflation.

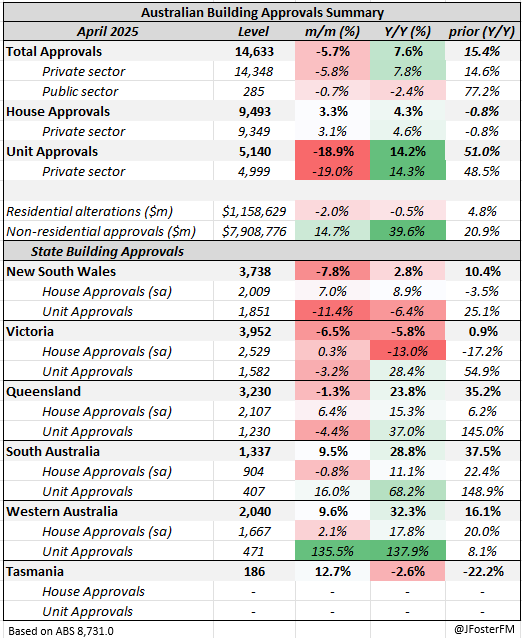

In Australia, April's CPI report showed headline inflation held at a 2.4%yr pace in the ABS's monthly gauge, in line with the more comprehensive quarterly series from Q1 (see here). Although trade developments remain the most relevant factor for $AUD exposures, the data front has Q1 economic growth figures coming up next week. My preview discusses the relevant dynamics here, with growth of around 0.4% in the quarter expected. Household consumption remains subdued as highlighted by a soft outcome of -0.1% for retail sales in April (see here). Recent momentum in dwelling approvals is now retracing (-5.7% in April) as strength in the higher-density segment is unwinding (see here).