Concerns over the health of the US consumer and ongoing uncertainty over tariffs remained the key macro themes in another broadly risk-off week in markets. Sentiment has soured towards to the Mag 7 names in the US, sending the Nasdaq to its largest weekly decline since September last year - even after a rebound in Friday's session. Asian equities were also hit hard, but Europe defied the weakness again. Growth worries have put Fed rate cuts back on the radar, driving Treasurys to rally across the curve; the 2-year trades at lows since last October and the 10-year sent back to early December levels. The overall backdrop was a tailwind to the USD.

The recent softening in the US data flow was put firmly in the spotlight after the Atlanta Fed's tracking estimate of Q1 GDP was reported at -1.5%. This has put added focus on next week's payrolls report where a weak number could drive a further risk-off reaction across markets. With the Fed's preferred inflation measure - the core PCE deflator - softening from 2.9% to 2.6%yr in January and consumer spending falling in the month in nominal (-0.2%) and real terms (-0.5%) - despite a 0.9% rise in personal incomes - markets have repriced to discount almost 3 rate cuts through the remainder of 2025.

In the euro area, the ECB is expected to cut rates at next week's meeting as focus in the meantime has remained on the neutral rate. The neutral rate - a theoretical concept for the level of rates that neither slows nor speeds up growth - has been in discussions at the ECB in recent times as the easing cycle has continued. A recent paper put out by the ECB estimated the neutral rate in the 1.75-2.25% range, implying that rates at the current 2.75% level remain restrictive. But as the account of the January meeting revealed, discussions are starting to stir that rates may be closer to a level that can no longer be assessed as restrictive. Executive Board member Schnabel - one of the leading voices in the discussion - outlined in a speech this week that structural factors are pushing up estimates of the neutral rate, a reverse of the pre-pandemic era where estimates were being persistently being lowered.

Australia's CPI report for January had few implications for RBA rates pricing, with a second rate cut unlikely to occur before the Board's May meeting. According to the ABS's monthly CPI indicator, headline inflation was 2.5%yr in January, an unchanged pace from December against an expected rise to 2.6%yr (reviewed here). The measures of underlying inflation firmed slightly: trimmed mean up from 2.7% to 2.8%yr and CPI excluding volatile items and holiday travel now 2.9%yr from 2.8%. The monthly indicator gives only a partial update of prices within the CPI basket, with the RBA's policy decisions guided by the comprehensive quarterly report. Of the prices that were updated at the start of the year, electricity (8.9%m/m) could pose upside risk to quarterly inflation with government rebates winding down.

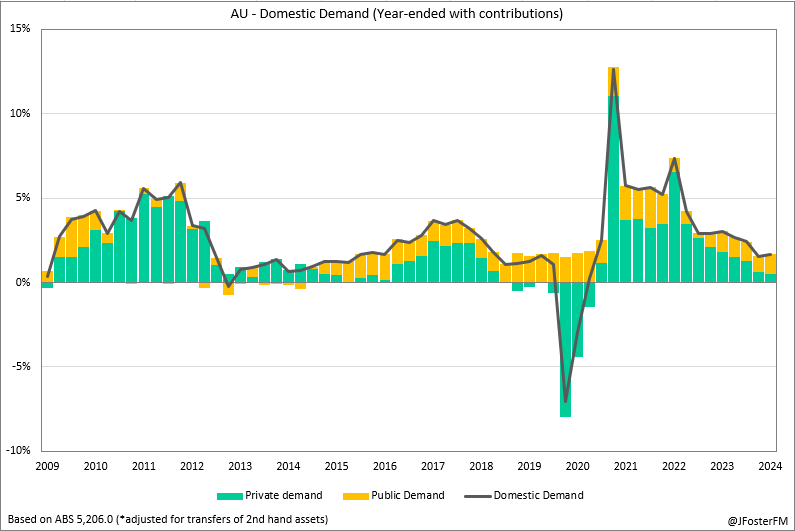

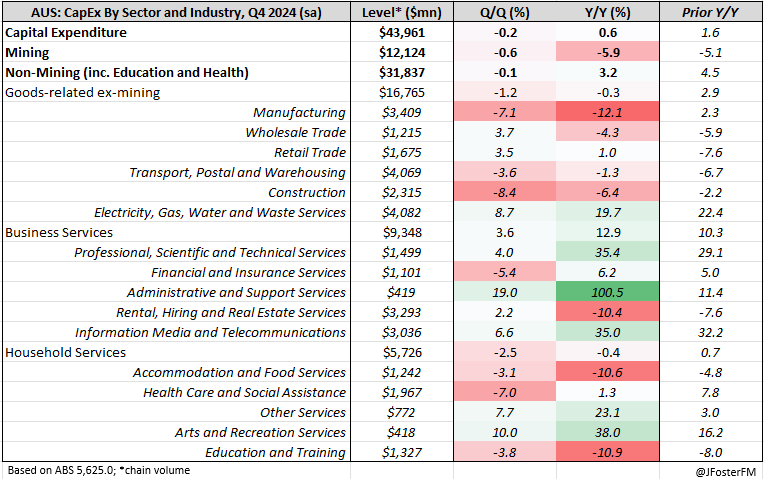

The highlight in Australia next week is the Q4 National Accounts, which are expected to confirm that quarterly GDP growth remained subdued at around 0.3%. My preview of the National Accounts gives a detailed overview of the key themes to watch out for, most notably an uptick in consumer spending through the Black Friday sales, spurred on by fiscal support, and ongoing strength in public demand (see here). Partial indicators for GDP released this week were mixed. Construction activity rose 0.5% in Q4, a modest outcome but with signs that the long-running malaise in the residential sector (0.9%) may be abating (see here). Capital expenditure by private sector firms has plateaued over the past year and contracted slightly (-0.2%) in Q4 (see here). Weakness in non-residential construction and a slowing in equipment spending were the key dynamics.