Australia's March quarter National Accounts are out this morning (4/6). Growth in the domestic economy was soft in 2024 as consumer demand was well contained under cost-of-living pressure and earlier RBA rate hikes. Public sector spending and investment have underpinned growth and employment for more than a year, helping to offset weakness in private demand. These dynamics remained broadly in place in early 2025, while adverse weather events also weighed on growth. Estimates sit around 0.3-0.4% for GDP growth in the quarter.

A recap: Domestic economy subdued, underpinned by public demand

Quarterly growth picked up at its fastest pace in 2 years as real GDP expanded by 0.6% in the December quarter, lifting annual growth from 0.8% to 1.3%. Despite this, underlying momentum in the economy has been subdued as cost-of-living pressures and higher interest rates have weighed on consumption and investment. The main driver of growth has been public sector spending, including household support measures and defence and infrastructure investment.

After contracting marginally in the prior two quarters, household consumption rebounded with a 0.4% rise in the December quarter, supported by discounting during the Black Friday sales. This drove goods consumption to its first quarterly increase (0.6%) in a year. Although declining in Q4 (-0.4%), dwelling investment picked up over the year (2.5%); however, the level of residential construction activity is flat since the RBA commenced its hiking cycle in Q2 2022. Business investment lifted by 0.5% in the quarter but stalled across 2024. Strength in IP and equipment have helped to offset weakness in non-residential construction.

Q1 preview: Global uncertainty adds to headwinds

Headwinds to growth from offshore intensified in early 2025 as impending tariffs from the US administration ramped up uncertainty around global trade. Quarterly growth across OECD economies slowed from 0.5% to 0.1% in the March quarter, its weakest outcome since the pandemic. Trade activity brought forward to front run tariffs had varying effects on growth at the country level; in the US, a surge of import orders swung GDP into contraction in the quarter (-0.1%), but growth picked up in the euro area (0.3%) and UK (0.7%) supported by exports bound for the US market. This also boosted growth in China, though it still slowed from 1.6% to 1.2% in the quarter as momentum in the domestic economy remained soft.

In Australia, growth through the early months of the year looks to have remained subdued. The RBA provided some support to demand by commencing its easing cycle with a 25bps cut to the cash rate in February, with data later confirming inflation returned to its 2-3% target band in the March quarter. Consumer sentiment showed signs of improving following the rate cut, but it has been stuck at pessimistic levels for 3 years now.

Economic activity in the March quarter was partly affected by adverse weather. Cyclone Alfred impacted south east Queensland and northern New South Wales in early March, while Cyclone Zelia in northern Western Australia disrupted resources shipments in mid-February.

Summary of key dynamics in Q1

Household consumption — Has been slow to respond to improving real incomes as inflation has cooled, and with the labour market remaining robust. The RBA's February rate cut and follow-up move in May will take time to help turn the tide. Retail sales volumes stalled in the quarter, pulling back after rising strongly last quarter (0.8%) due largely to Black Friday discounting.

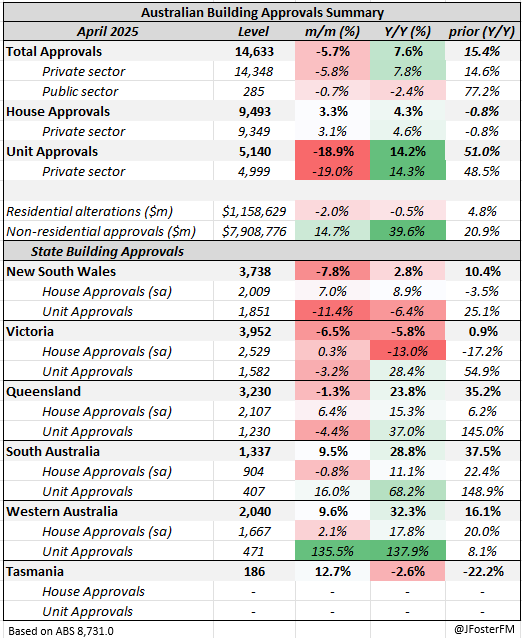

Dwelling investment — Looks set to rebound from a contraction in Q4, renewing its earlier momentum from 2024. Partial data indicated both new home building and alteration work advanced over Q1.

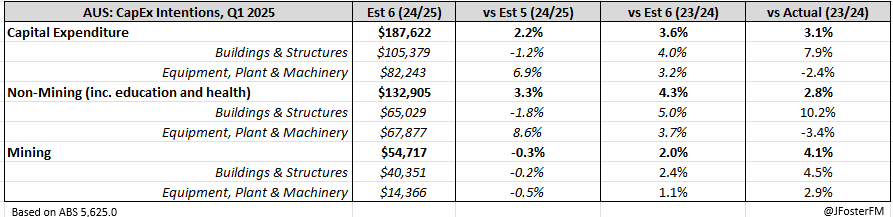

Business investment — Momentum stalled over the course of last year and appears to have been weak in early 2025, with private sector capex recording a small decline in Q1. Business surveys have highlighted margin pressures and weak demand as key concerns, while elevated uncertainty has weighed on confidence.

Public demand — Lost momentum in the quarter as government spending flatlined and investment softened, despite a large pipeline of activity.

Inventories — A modest add of 0.1-0.2ppt to GDP looks likely. No noticeable volatility in the partial data that pointed to the effects of global trade uncertainty.

Net exports — Aside from isolated examples (most notably non-monetary gold) frontrunning of the US administration's liberation day tariffs was not broadly evident in the trade data, unlike many other countries. Net exports to weigh modestly on GDP growth in Q1 (-0.1ppt).