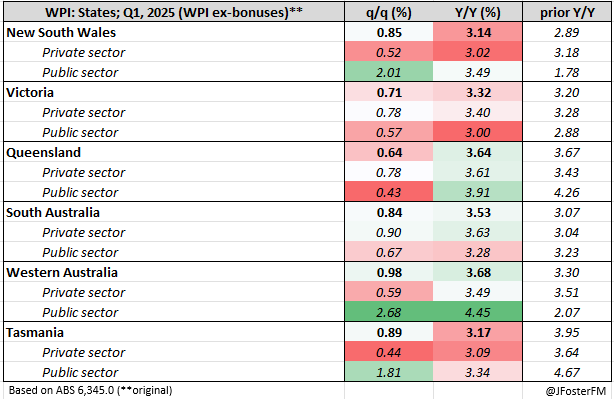

Australia's latest monthly employment report for April is due this morning local time (1130 AEST). Wages growth surprised a little to the upside in yesterday's report for Q1, but a 25bps rate cut from the RBA on May 20 still holds sway with markets. With core inflation back in the 2-3% target band and wage pressures having cooled substantially from their cycle peaks, a relatively calm report today likely gives the RBA the green light to cut next week.

April preview: Calmer waters expected after recent volatility

After a volatile start to the year that has been influenced by seasonality, increased retirements and the disruptions from ex-tropical cyclone Alfred, a more sedate read on labour market conditions is expected today. The median forecast is for employment to rise by 22.5k, with estimates ranging between 15k on the low side up to 40k top side. Employment lifted by 32.2k last time out in March. Expectations are that the unemployment rate holds at 4.1% (range: 4.1% to 4.2%), but much will depend on what happens with the participation rate, which at 66.8% is off recent record highs.

Following back-to-back outcomes where employment undershot expectations in February and March, the question is whether we see some payback in April with an upside result. History doesn't offer much of a steer given that employment outcomes in April in recent years have been mixed. Add to this the recent volatility in the series and today's report shapes as a bit of a wildcard. My guesstimate is for a 35k increase in employment.

March recap: Employment rebound falls short after February shock

Employment increased by a net 32.2k in March (full time 15k/part time 17.2k), a decent result in isolation but short of the 40k rise expected after February's shock 57.5k decline. Across the first quarter of the year, employment was subdued rising by just 6.5k - its weakest quarterly result since Q3 2021.

The national unemployment rate was little changed, though it was rounded up in reporting to 4.1% in March from 4% in February. Nonetheless, unemployment remains historically low and has averaged 4.1% over the past year. Meanwhile, the levels of underemployment at 5.9% and underutilisation at 9.9% have actually declined on 12 months ago, confirming this remains a robust labour market.

Perhaps the most significant surprise in March came on the supply side. The participation rate held at an unchanged 66.8%, the level down from record highs (67.2%) at the start of the year on the back of a wave of retirements. A decline in the size of the labour force appeared to weigh on hours worked in February (-0.4%), while in March hours worked fell further (-0.3%) with the disruptions caused by ex-tropical cyclone Alfred in Queensland (-3.8%) playing a role.