Australia's trade surplus reset to a new record high in May as export earnings continued to surge on the back of strength in key commodities. Rising national income is helping to offset the economic impact of the escalation in global oil prices.

International Trade — May | By the numbers

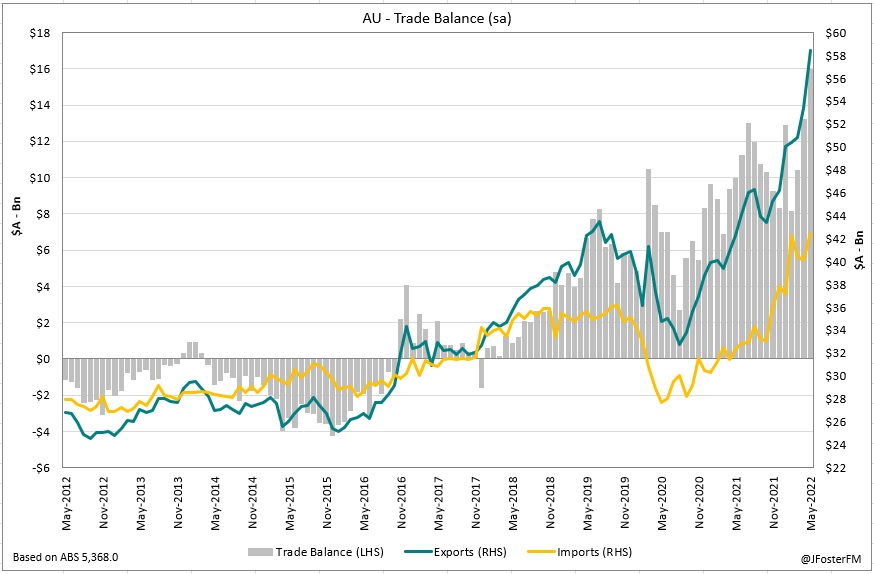

- Australia's trade surplus came in well above expectations in May ($10.8bn), widening out to $16bn from $13.2bn in April (revised from $10.5bn).

- Exports accelerated by 9.5% in the month to $58.4bn to be up by 38.1% over the year. This followed a sharply upgraded gain in April, revised to 5% from 1%.

- Imports posted a 5.8% rise to $42.4bn taking out the previous record high in April. Annual growth firmed from 27.4% to 31.4%.

International Trade — May | The details

Australia's position as a major commodity exporter has seen its monthly trade surplus elevating to $16bn in May, almost double its level from February prior to the Russian invasion of Ukraine. With the war driving a surge in commodity prices, the trade surplus has stepped sequentially higher over the period, lifting from $8.1bn to $10.4bn in March, then to $13.2bn in April and now $16bn in May.

Monthly export earnings are close to pressing $60bn after surging by 9.5% in May alone, taking the overall increase since February to nearly 16%. Exports were driven by a 9% lift in non-rural goods in May, centred rises in the major commodities: coal 20.4%, LNG 11.8% and iron ore 2.8%. With May's surge coming on the back of large increases in the prior two months, coal overtook iron ore as the nation's highest value export, the last time this happened was back in 2009. ABS data suggested the strength was driven by a rebound in shipment volumes after falling in April. Non-monetary gold (71%m/m) also boosted monthly exports.

Rural goods lifted by another 3.6% in May to $5.6bn, a record high. Strong offshore demand, rising prices and favourable weather conditions have seen earnings from rural goods surge since mid-2020.

The reopening of the international border earlier in the year is starting to see services exports (4.8%m/m) rise sustainably from their lows of the pandemic.

Imports rebounded from soft outcomes in the prior two months lifting by 5.8% in May to $42.4bn. Increases were broad based but were led by intermediate goods (9%) as fuel imports continued to surge reflecting high oil prices, rising by 22.9% in the month to be up by 151% over the year.

Pointing to the easing of some of the constraints holding up global supply chains, new vehicle imports lifted by 18.5%m/m and machinery and industrial equipment advanced by 6.5%m/m; the former driving consumption goods to a 5.4% rise in the month and the latter pushing up capital goods by 3.2%m/m. Services imports (4.1%m/m) remain on the recovery path following the easing of restrictions on offshore travel.

International Trade — May | Insights

Surging commodity prices continue to drive widening Australian trade surpluses. The war in Ukraine and its spillover impact on commodity prices has been a positive terms of trade shock for Australia and other commodity exporting nations. Australia's terms of trade hit a record high in the March quarter and are very likely to reset that benchmark in the June quarter, providing a buffer against the surge in oil prices. However, despite these factors, the Australian dollar has weakened sharply against the US dollar in 2022 (down by around 6%) reflecting concerns over the global economic growth outlook and the aggressive rate hiking cycle from the Federal Reserve.