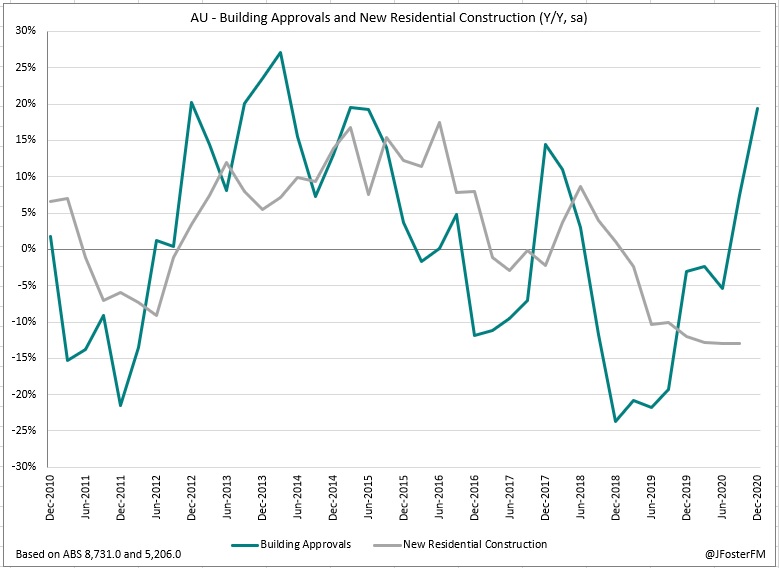

Chart of the week

The minutes from February's RBA meeting released this week emphasised the Board's commitment to keeping policy settings very accommodative until spare capacity has reduced from its elevated levels. Most notably, the decision to expand its bond purchase program by a further $100bn was justified to ward off "unwelcome significant upward pressure on the exchange rate" that would have otherwise emerged if the RBA went against the trend of increased bond-buying by other major central banks. The main point of speculation in the markets is currently around the future of the 3-year yield target, with some segments speculating the Board may adjust or even remove the policy later on this year, though on the available evidence it would appear that conditions in the economy over the coming months would need to resolve considerably to the upside of expectations for this to occur. On the current outlook, the Board's expectation is that its employment and inflation objectives are some years away and on that basis, it considers that "it would be premature to consider withdrawing monetary stimulus".

— — —

Offshore this week there were some signs of concern that the reflation theme could be self-limiting as yield curves steepened sharply over the week. Whereas the recent rise in long-end yields has been driven by the expectation for higher inflation to build as vaccines enable more sustainable reopenings, this faded over the week leading to real rates, which are still deeply negative, moving a little higher. With the inflation outlook key for markets, communications from the major central banks pointed to a nuanced stance. The minutes from the US Federal Reserve's FOMC meeting in late January outlined that inflation would be moving gradually higher as the effects of the pandemic dissipate. However, in the near-term, some members foresaw price levels spiking higher to be above its 2% objective, largely reflecting temporary factors. In this context, the line from the FOMC is that it will be important to differentiate between "one-time changes in relative prices and changes in the underlying trend for inflation". While the Committee has moved to a less pessimistic view on conditions over the medium term, it still assesses that risks and uncertainties around the outlook for the economy are elevated amidst the pandemic and in light of this there are no clear signs that it is contemplating tapering its asset purchases from its current $120bn/mth rate. Indeed, not only does the FOMC want to see complete recovery from the pandemic shock, it is then aiming for conditions to strengthen substantially before policy accommodation will be removed. Fiscal support will also play a key role in helping the economy get back on track, as highlighted the effect of recent stimulus cheques driving retail sales sharply higher in January with a 5.3% rise. The result may have been overstated to some extent by weakness in recent months (sales fell in each of the past 3 months), but the stimulus cheques appeared the catalyst in turning the tide. Control group sales (a narrower measure of underlying demand) outperformed the headline increased with a 6.0% surge in the month.

Switching the focus to Europe, the account of the meeting by the ECB's Governing Council in January also contained key insights around inflation dynamics. The Governing Council discussed the possibility that inflation could rise more sharply than its projections implied in 2021 reflecting a combination of higher energy prices, the unwinding of the temporary VAT cut in Germany, and the return of pent-up demand once restrictions were eased. The key point communicated in January's account was that "a temporary boost to inflation should not be mistaken for a sustained increase". The major emphasis outlined by the Governing Council at its previous meeting was that it will aim to maintain "favourable financing conditions" throughout the recovery. In this global reflation environment, there are two main concerns for the ECB in this effort. Firstly, it was noted that monitoring the effect of upward pressure on bond yields on financing conditions "would be an important task", and secondly, a stronger currency via a weaker US dollar "might have negative implications for euro area financial conditions". As such, it is understandable that the Governing Council continues to note that "all instruments needed to remain on the table". The latest flash PMI readings for the bloc remained consistent with an economy still shuttered to a great extent as activity registered its 4th consecutive contractionary result coming in at 48.1 on the composite index in February. But while the services sector (44.7) remains severely hampered by the shutdowns, the manufacturing sector (57.7) is helping to attenuate its impact on the economy, reflecting shifts towards more goods-based consumption and strengthening demand offshore.