Labour Force Survey — June | By the numbers

- Employment on net increased by 210.8k in June (seasonally adjusted), a record monthly rise and well ahead of the consensus forecast of 100.0k. In May, employment was revised to show a larger fall of 264.1k from the -227.7k figure reported initially.

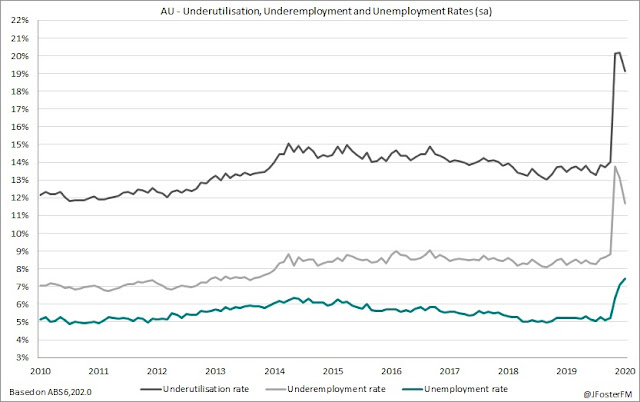

- Headline unemployment increased by more than expected rising from 7.1% to 7.4% (vs 7.3% expected). Underemployment declined from 13.1% to 11.7%, bringing the underutilisation rate down from its record high of 20.2% to 19.1%.

- The participation rate lifted by 1.3ppt to 64.0% to come in above consensus (63.3%).

- Aggregate hours worked surged by 4.0% in the month to around 1.66bn hours, slowing the pace of contraction in annual terms from -9.2% to -5.7%.

Labour Force Survey — June | The details

The reopening process out of the shutdown resulted in 210.8k coming back to the economy in the month of June. In context, this represents 24% of the jobs that fell victim to the pandemic and the actions taken by the authorities to contain the spread of the virus being restored. All of the gain in employment in June came from the part-time segment (+249.0k) as full-time work continued to fall (-38.1k).

The reopening process out of the shutdown resulted in 210.8k coming back to the economy in the month of June. In context, this represents 24% of the jobs that fell victim to the pandemic and the actions taken by the authorities to contain the spread of the virus being restored. All of the gain in employment in June came from the part-time segment (+249.0k) as full-time work continued to fall (-38.1k).

Ahead of the pandemic, Australia's rate of workforce participation had been at its highest levels on record north of 66%. The shutdown and easing of the mutual obligation requirement associated with the receipt of the JobSeeker support payment saw this decline precipitously to its lowest level in two decades at 62.7% by May. In June, workforce participation lifted by 1.3ppt to 64.0% as more Australians were able to return to work and some mutual obligation requirements started to be reintroduced. As a result of the uptick in participation, the unemployment rate moved up from 7.1% to 7.4% to its highest level since November 1998. Clearly, with participation still well below its pre-pandemic level more upward pressure will be placed on the unemployment rate.

Due to the nature of this pandemic where shutdowns were implemented, the dislocation to the labour market has been best reflected by its impact on hours worked. The reopening of the economy saw total hours worked rebound by 4.0% in June to around 1.66bn hours (-5.7%yr). This is down by 6% from its level in February.

Accordingly, with more hours being worked, the rate of underemployment was brought lower from 13.1% to 11.7%. Combining the unemployed and underemployed, the rate of underutilisation as a share of the labour force eased from 20.2% to 19.1%. Both of these measures continue to provide a more accurate depiction of current dynamics in the labour market than the unemployment rate.

Labour Force Survey — June | Insights

The upside result on the employment number of 210.8k was a positive, but not unexpected and consistent with the reopening narrative centring entirely on part-time employment that had been hit hardest by the shutdown through April into May. Over the period, employment in the part-time segment fell by 533.7k compared to a 337.8k contraction in full-time work. The easing of restrictions that occurred progressively from early May started to allow workers, particularly those in front-facing industries to return to their jobs, albeit in a restricted capacity, leading to an increase in hours worked across the economy. The very significant challenges that are ahead were best highlighted in Tuesday's NAB Business Survey. Capacity utilisation has fallen to well below average levels across several major industries and with efforts to contain the pandemic likely to be ongoing, repairing the extent of the damage sustained to the labour market will be very difficult indeed. Clearly, the return to shutdown in Melbourne and elevated concerns about the virus more widely will make this even harder.

The upside result on the employment number of 210.8k was a positive, but not unexpected and consistent with the reopening narrative centring entirely on part-time employment that had been hit hardest by the shutdown through April into May. Over the period, employment in the part-time segment fell by 533.7k compared to a 337.8k contraction in full-time work. The easing of restrictions that occurred progressively from early May started to allow workers, particularly those in front-facing industries to return to their jobs, albeit in a restricted capacity, leading to an increase in hours worked across the economy. The very significant challenges that are ahead were best highlighted in Tuesday's NAB Business Survey. Capacity utilisation has fallen to well below average levels across several major industries and with efforts to contain the pandemic likely to be ongoing, repairing the extent of the damage sustained to the labour market will be very difficult indeed. Clearly, the return to shutdown in Melbourne and elevated concerns about the virus more widely will make this even harder.