Australia's economic expansion got back on track in the December quarter after state-based lockdowns during the Delta wave of Covid-19 were eased. These lockdowns drove a 1.9% contraction in the previous quarter, but real GDP rebounded by 3.4% in Q4, broadly in line with market expectations, firming the pace of growth to 4.2% through the year.

Over the first half of 2021, GDP increased at a robust 2.7% pace and was 1.9% above its pre-pandemic level, indicating that the expansion from the Covid recession was well underway. The Delta lockdowns and emergence of supply constraints disrupted this momentum, with GDP backsliding to its pre-pandemic level in the September quarter. The strong 3.4% rebound in Q4 has re-established the earlier momentum in the expansion, with GDP rising to 3.4% above its pre-pandemic level at the turn of the year.

Offshore, conditions were supportive of Australia's rebound in Q4. Tightening labor markets and fiscal and monetary stimulus had continued to support robust demand. GDP in advanced economies was either above or in line with pre-pandemic levels by the end of 2021. Constraints in global supply chains remained prevalent, contributing to inflation pressures. Meanwhile, GDP growth in China picked up pace after slowing sharply in Q3, with manufacturing and exports benefitting from the global recovery.

In Australia, state-based lockdowns in New South Wales, Victoria and the ACT were lifted early in Q4 as key vaccination thresholds were achieved. The effects of eased restrictions, the rollout of the vaccine and pent-up demand led to a very sharp rebound in mobility indicators in Sydney and Melbourne, reaching their highest levels since the outset of the pandemic, while average mobility in the other capitals also increased.

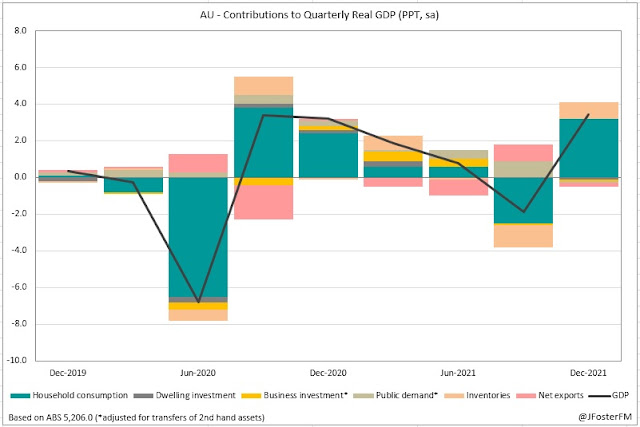

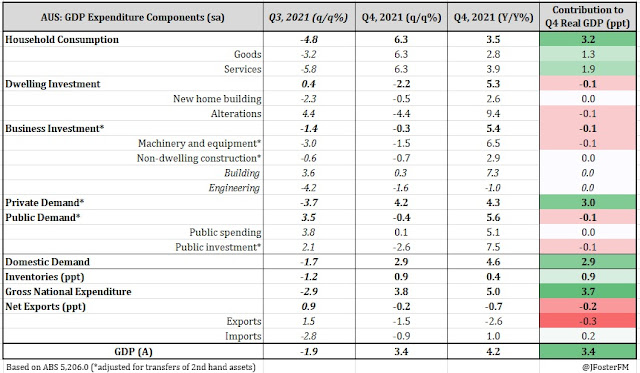

Australia's December quarter rebound in GDP of 3.4% was on par with the surge seen back in Q3 2020 after the national lockdown was eased; this despite the 1.9% fall in output during the Delta outbreak being much less severe than the recession the initial wave caused. Household consumption drove the recovery, contributing 3.2ppts to quarterly GDP. This was led by discretionary spending (2.6ppts) as entertainment and hospitality venues and shopping centres reopened and as travel restrictions started easing. Robust sentiment and a tightening labour market encouraged households to spend out of accumulated savings, with the household saving ratio falling from 19.8% to 13.6%, still a very elevated level. These factors contributed to rising inflation pressures in the quarter, but with the main driver still being pandemic-related supply constraints rather than high wages growth.

Reflecting the headwinds of supply constraints, both business investment (-0.1ppt) and residential construction activity (-0.1ppt) contracted in the quarter, driving weakness in private investment. Inventories were also at low levels due to being held back by shortages, though there was some rebuilding during Q4, contributing 0.9ppt to activity. Net exports deducted 0.2ppt from quarterly GDP as the pandemic continues to disrupt global trade. Travel restrictions have crunched Australia's exports by 12.8% over the Covid period, while imports are down by 8.6% from the end of 2019. Eased border restrictions will be a welcome relief in 2022. In addition to reopening effects, the nation's rural sector continued to support the economy, with favourable conditions facilitating meeting strong domestic and global demand. Farm GDP surged by 11.2%q/q and was 20.9% higher through the year.

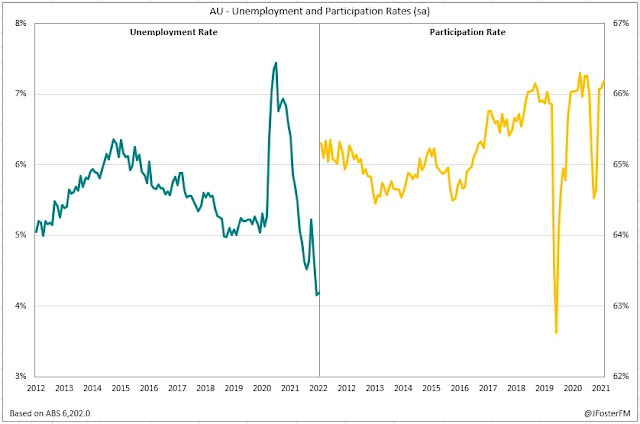

Economic conditions supported a recovery in the labour market in Q4. With employment and hours worked returning to their pre-Delta levels, spare capacity in the labour market tightened considerably. The national unemployment rate fell to 4.2% in December, its lowest since 2008, while labour force participation was close to record highs.

In response to the robust rebound in the economy and the tightening in the labour market, the RBA wound up purchases in its QE program at the February meeting. Rising inflation and upgraded forecasts prompted Governor Philip Lowe to put the possibility of raising rates in 2022 on the table, though the Board has repeated it will not act pre-emptively; instead taking a patient approach in assessing the durability of price pressures, with wages growth the key factor in determining the outlook. Australia looks to be coming through the Omicron wave with resilience despite significant disruptions in January, suggesting the pandemic is a fading headwind to the economy, particularly with the borders now reopened. All in all, with monetary policy to remain supportive in the push towards full employment, indications from the Q4 national accounts are that the Australian economy is set up to perform strongly in 2022.

— — —

National Accounts — Q4 | Expenditure: GDP (E) 3.6%q/q, 4.1%Y/Y

Household consumption (6.3%q/q, 3.5%Y/Y) — After the lockdowns eased, household spending was resurgent rising by 6.3% in the quarter to be up by 3.5% through the year. Eased restrictions, robust sentiment, strong household balance sheets and a tightening labour market all supported the rebound in consumption.

The states reopening from Q3 lockdowns drove the resurgence in household spending: New South Wales 11.4%, Victoria 7.5% and the ACT 8.4%; but consumption was still short of returning to pre-pandemic levels. The expansion in household consumption across the other states and territories (those relatively unscathed by Delta) continued as growth accelerated to 1.6% in Q4 from 0.8% in Q3.

Nationally, the 6.3% rebound in Q4 saw household consumption recovering to 0.8% above its pre-pandemic level in Q4 2019. This was driven predominantly by discretionary consumption, which surged by 14.2% after being crunched by the lockdowns in Q3 (-11.2%). The reopening of entertainment & sporting venues and licensed premises supported a rebound in recreation & culture (17.1%q/q) and at cafes, hotels & restaurants (24.3%q/q). With people able to get and about again, and with non-essential retail reopening, clothing and footwear consumption bounced back strongly (41.6%q/q). Also seeing a rebound was transport services (48.5%q/q) as some domestic and international travel restrictions were eased; household goods (7.7%q/q); and other goods & services (mainly personal care services and effects) (9.0%q/q). Essential consumption lifted by 1.9% in the quarter, driven mainly by fuel (13.9%q/q) as mobility restrictions were wound back.

Both goods and services consumption posted rebounds of 6.3% in the quarter, with the latter coming back from a much larger fall in Q3 of 5.8% compared to a 3.2% contraction in goods. This meant that services spending made a more sizeable contribution to GDP growth in Q4 (1.9ppt) than goods consumption (1.3ppt). However, a significant imbalance in consumption patterns relative to pre-Covid levels persists: goods consumption is vastly higher (8.8%) while services consumption is still well down (-3.9%).

Although employment and hours worked rebounded in the quarter, gross disposable income contracted overall (-0.5%q/q). The main factor was the unwinding of the fiscal support payments that were in place during the lockdowns, with social assistance benefits -10.9%q/q. Adjusting for inflation, real gross disposable income was down 1.3%q/q but had expanded over the year (2.7%). The 6.3% rebound in household consumption came despite this softer picture for household income. The key was that the household saving ratio had surged during the Q3's lockdowns to a very elevated 19.3%. Robust sentiment, pent-up demand and a tightening labour market meant that households were confident to spend out of accumulated savings. As a result, the household saving ratio declined by 6.2ppts to 13.6% in Q4. This is still well above the decade average leading up to the pandemic (around 6%), indicating households retain a large amount of excess savings.

Dwelling investment (-2.2%q/q, 5.3%Y/Y) — Residential construction activity lost momentum over the back half of the year (-1.8%), with lockdown disruptions and capacity constraints from materials and labour shortages stalling the stimulus-driven upswing seen through the first half (7.2%). In Q4, dwelling investment contracted by 2.2% but was still 5.3% higher through the year and up by 4.7% on a pre-pandemic comparison.

Conditions in the established housing market were boosted by the resumption of activity in the key Sydney and Melbourne markets as restrictions were eased. This supported a 4.4% rise in national housing prices during the quarter for an annual increase of around 22%. Accordingly, ownership transfer costs — fees associated with real estate transactions — had surged over the year (21.5%) but contracted in Q4 (-3.7%).

Business investment (-0.3%q/q, 5.4%Y/Y) — After Q3's lockdown-related fall (-1.4%), business investment weakened further in the December quarter (-0.4%). This profile confirmed a loss of momentum over the second half of the year (-1.7%) from the upswing in the first half (7.3%), leaving business investment broadly in line with its relatively weak level seen prior to the onset of the pandemic.

In Q4, machinery and equipment spending failed to rebound (-1.5%) from the contraction in the prior quarter (-3%). The Delta lockdowns and associated disruptions had likely caused firms to delay some capital investment purchases, while global supply chain constraints had also weighed. Engineering work contracted for the second quarter running (-1.6%q/q) on residual effects from restrictions on the construction sector during the Delta wave in Victoria. Against this weakness, commercial building work had increased pace over the second half of the year, supported by warehousing.

Despite the recent headwinds, the latest ABS Capital Expenditure survey reported an upgraded outlook for firms' investment plans. Expectations for a strong economy, government tax incentives and accommodative financing conditions argue for business investment to regain momentum in 2022, though geopolitical turmoil could have implications.

Public demand (-0.4%q/q, 5.6%Y/Y) — Robust growth in public demand has been a key support to the Australian economy throughout the Covid period but moderated in Q4 (-0.4%). Consumption spending (0.1%q/q) has been boosted by the pandemic response, including the rollout of the vaccine. Underlying investment declined in the quarter (-2.2%) but is supported by a vast pipeline of government infrastructure projects.

Inventories (+0.9ppt in Q4, +0.4ppt yr) — After a sizeable drawdown in Q3, inventories were rebuilt to some extent in the December quarter and added 0.9ppt to GDP, though they still remain at low levels as global supply chain pressures persist. A rise in wholesale inventories was the main contributor due to increased demand for fuel as the Delta-affected states reopened from lockdowns. Manufacturing inventories were also increased to meet the rebound in demand for household durables.

Net exports (-0.2ppt in Q4, -0.7ppt yr) — Net exports weighed modestly on activity in Q4, subtracting 0.2ppt from GDP. Exports declined by 1.5% in the quarter to be 12.8% below pre-Covid levels. Softer global demand and shipping constraints were a headwind for resources exports in Q4 (-1.5%). Import volumes contracted by 0.9% in Q4 and were down by 8.6% on their pre-Covid level. Constraints in global production from the pandemic and semi-conductor shortages continued to hold back imports of new vehicles and also weighed on machinery and industrial equipment purchases in the quarter.

— — —

National Accounts — Q4 | Incomes: GDP (I) 3.4%q/q, 4.4%Y/Y

The December quarter real GDP income estimate came in at 3.4%q/q, rebounding from Q3's 1.7% contraction to be up by 4.4% through the year. National income rebounded in line with the recovery in the economy, with nominal GDP rising by 3.4% in Q4 (from -0.6% in Q3), taking it to 11.1% above its pre-pandemic level.

National income has surged higher from the depths seen during the initial 2020 lockdown and was only temporarily disrupted by the Delta setback. A strong economic recovery and elevated commodity prices have been the driving factors. In Q4, the latter started to come off as the iron ore price retraced, though the effect was attenuated by increases in prices of other export commodities (such as LNG, coal and rural products). This held export prices to just a 0.4% rise in the quarter, while import prices accelerated at a 5.8% pace amid global supply chain pressures. As a result, the nation's terms of trade contracted by 5.1% in the quarter, retracing from a record high.

As the lockdowns were wound back, the labour market tightened considerably as employment and hours worked rebounded. This drove compensation of employees up by 2% in the quarter — its strongest outturn since the national reopening in Q3 2020 — accelerating annual growth from 4.6% to 5.3%.

A rebounding economy also supported company profits during Q4. Private non-financial corporations operating surplus firmed by 0.4%q/q, rising to be 9.6% higher through the year. Financial corporations operating surplus advanced at a stronger pace in the quarter (1.2%) but is running at a softer year-over-year pace at 5.2%. Small business profits built on Q3's surge (8.2%) when fiscal payments were a key support during the lockdowns. Gross mixed income lifted by a further 3% in the quarter to 11.7%Y/Y.

Overall, total factor income was up by 1.5% in the December quarter, well down on the 3.4%q/q advance in nominal GDP. Movements in the two are usually closely aligned but have deviated over the Covid period as government support payments have flowed. In Q4, fiscal support measures were wound back after the lockdowns ended, reflected by a 29.2%q/q rise in taxes less subsidies, explaining the slower rise in total factor income.

— — —

National Accounts — Q4 | Production: GDP (P) 3.3%q/q, 4.2%Y/Y

In the December quarter, the GDP production measure lifted at a 3.3% pace after contracting by 1.8% in Q3, with annual growth ticking up to 4.2%. Reflecting the easing of the lockdowns, the services sector of the economy saw the largest rebound in the quarter, from -2.3% to 4.9%, to be 4.1% above its pre-pandemic level. A more moderate upturn was seen in the goods sector, from -1.3% to 1.8%, and was just above its pre-pandemic level (0.3%).

In the services sector, household services swung from a lockdown-affected Q3 where gross value added (GVA) contracted by 5.6% to a 7.1% reopening rebound in Q4. This drove the sector back into expansion relative to its pre-pandemic level (+3.4%) after collapsing below that benchmark in Q3 (-3.4%). Driving the rebound was the accommodation and food industry (26.1%q/q) as restaurants and licensed venues in New South Wales, Victoria and the ACT reopened and travel restriction eased; arts and recreation (8.2%q/q) with entertainment venues able to trade again; and other services (15.4%q/q) supported by personal care and vehicle repair services. Business services accelerated by 3.4% from a flat Q3, driving GVA to 4.7% above its pre-Covid level. Professional services expanded by 5.3%q/q on strength in pre-construction and consulting services. Meanwhile, administration and support posted a 5.1% rise in the quarter, with travel agency services back in demand.

In the goods sector, goods distribution rebounded from Q3's fall (-4%) rising by 4.7% in Q4 to be 1.2% above its pre-Covid level. The retail industry surged by 7.4% as in-store retail reopened in New South Wales, Victoria and the ACT. A 3.5%q/q rise in the wholesale industry was driven by a record grain harvest and strong demand for agricultural and telecommunications equipment. The transport industry was up 3%q/q due to strength in courier services to facilitate online shopping and from an easing in travel restrictions. Goods production lifted modestly by 0.4% in Q4 and was 0.2% below its pre-Covid level. The manufacturing industry advanced by 1.8%q/q on the back of the post-lockdown rebound in household consumption. Output in the construction industry expanded by 1.9%q/q, boosted by the ending of the lockdown restrictions on projects at residential homes in New South Wales in Q3; however, shortages of materials and labour remained a headwind.

— — —

National Accounts — Q4 | Prices

— — —

National Accounts — Q4 | Productivity

The reopening of Delta-affected states saw hours worked across the economy rebounding by 4.3% in Q4 but were still 0.9% below their pre-pandemic level. In the market sector, hours worked lifted by 5.7%q/q following Q3's 6.1% contraction, still leaving a sizeable shortfall to their pre-pandemic level of -2.2%. With the hours worked measures rising by more than the increase in output in the quarter (3.4%), GDP per hour worked contracted by 0.8% (2%Y/Y) and by -2% in the market sector (2%Y/Y). Adjusting labour costs for productivity and inflation, real non-farm unit labour costs declined by 0.2% in the quarter, with a base effect slowing the annual pace to 0.7%, to be around its pre-pandemic pace.

— — —

National Accounts — Q4 | States

The New South Wales economy rebounded sharply in Q4. State demand had collapsed to 3.3% below its pre-pandemic level during the Delta lockdown, but the 6.7% rebound in Q4 sent it to 3.1% above its level seen at the end of 2019. Household consumption surged by 11.4%q/q as discretionary spending rebounded following the reopening of hospitality venues and retail centres, more than reversing Q3's 10.8% contraction. Business investment bounced back by 5% q/q, returning back above pre-pandemic levels as equipment spending in the hospitality industry picked up to facilitate the reopening and as restrictions in the construction sector eased. Residential construction activity was also rebounding (3.3%q/q).

In Victoria, state demand bounced back from Q3's 1.5% contraction, rising by 3.7% in the quarter. The state has been battered by rolling lockdowns throughout the Covid period but Q4's rebound saw state demand rising to be 3.1% above its pre-pandemic level. Household consumption lifted by 5.7% in the quarter as spending at hotels, restaurants and at the shops benefitted from eased restrictions. Both residential construction (-2.3%) and business investment (-2.4%) contracted in Q4, with constraints from materials and labour shortages holding up progress in construction work. Public demand lifted by a further 0.9%q/q to be up by 7.6% through the year, boosted by the state government's pandemic response.

The other states recorded much more modest changes in Q4, largely unaffected by the Delta wave. Queensland state demand was flat in the quarter but was up 6.1% on its pre-pandemic level. A pick-up in household consumption (2%q/q) led by discretionary services and new vehicles was offset by declines in business investment (-2.6%q/q) as work on renewable energy projects moderated and in residential construction (-4.4%) with capacity constraints weighing. South Australian state demand firmed by 0.3%q/q, to be 5.9% above its pre-pandemic level. Household consumption accelerated to 1.4% from 0.3% in the prior quarter, with spending in discretionary services rising after the rollout of the vaccine. This was attenuated by falls in business investment (-2.3%q/q) following an earlier surge, which is still 7.4% above its end-2019 level, and residential construction (-6.6%q/q) as alteration work pulled back after the HomeBuilder scheme wound down earlier in the year.

State demand in Western Australia was broadly flat in the quarter (0.1%) and was 6.3% above its pre-pandemic level. A broad-based rise in household consumption (1.5%) was weighed by weakness in residential construction (-2.9%q/q) and business investment (-2.7%q/q) amid capacity constraints with the state's border remaining closed over the quarter. Increased spending on infrastructure projects drove in 1% rise in public demand in Q4. Tasmanian state demand contracted by 1.5%q/q but was 8.2% above its level at the end of 2019, the strongest pre-Covid comparison of all the states. Supply constraints were headwinds for business investment (-11.4%q/q) and residential construction (-8.2%q/q), which more than offset stronger household consumption (0.5%q/q). Public demand also weighed (-0.9%q/q) as fiscal support was wound back.